Online food and grocery delivery startup Swiggy saw its growth drop in FY21 even as its grocery business expanded. The Bengaluru-based recently-turned decacorn had its overall income decline by more than 25% during the fiscal ended 2021.

Swiggy’s decline in scale is in line with the overall industry as its biggest competitor Zomato’s scale went down by 24% during the same period.

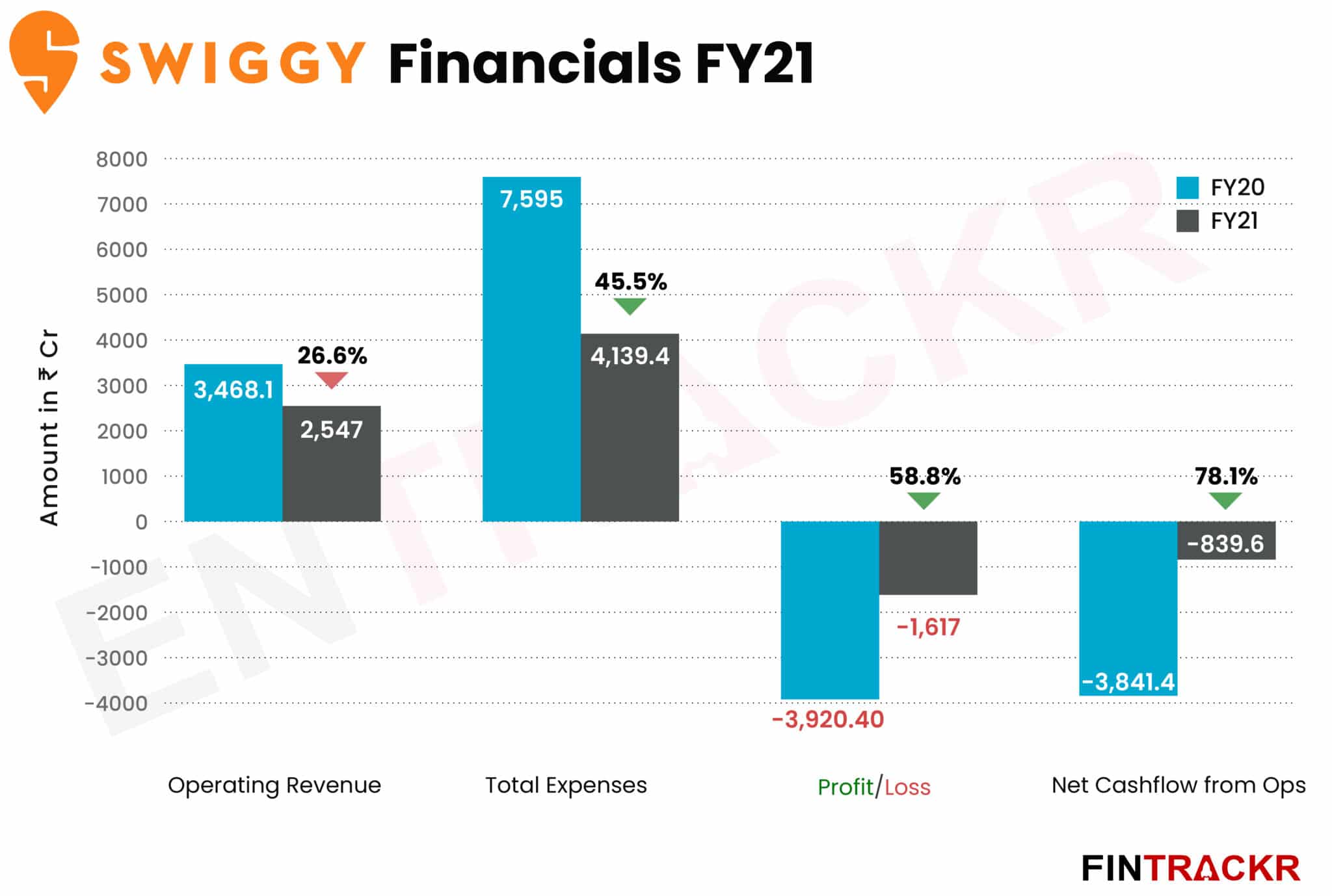

Swiggy’s revenue from operations dropped by 26.6% to Rs 2,547 crore in FY21 as compared to Rs 3,468 crore the company generated during FY20 while facing countrywide lockdown and restriction on delivery services for an extended period of time, regulatory filings show.

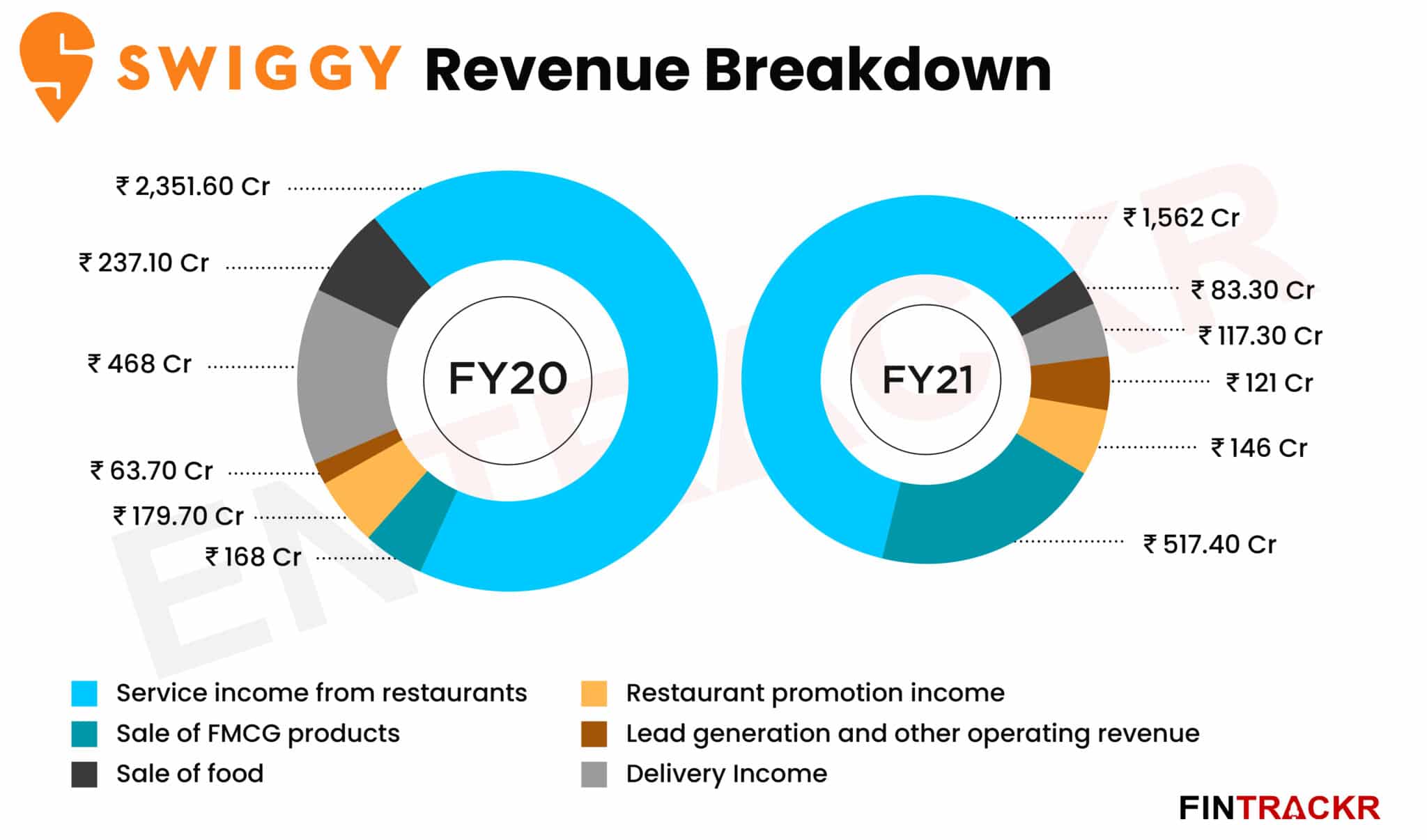

The food and grocery tech company collects service income from restaurants on its platform after completion of each order which accounts for 61.3% of total operating revenue. These collections dropped by 33.6% to Rs 1,562 crore in FY21 from Rs 2,351.6 crore earned in FY20.

Swiggy also charges a fee to promote restaurants on top of the discovery list and this income dropped by nearly 19% to Rs 146 crore in FY21 from Rs 179.7 crore in the preceding fiscal year (FY20).

This year, the delivery income earned by the company is recorded net of expenses, hence it dropped by 75% to Rs 117.3 crore in FY21 from Rs 468 crore during FY20. Lead generation and other related operating revenue grew nearly 90% YoY to Rs 121 crore during FY21.

Swiggy operates its own network of cloud kitchens under its private labels The Bowl Company, Goodness Kitchen, Breakfast Express and Homely. The sale of food from these private brands dropped by around 65% to Rs 83.3 crore during FY21 from Rs 237.1 crore in FY20.

With Swiggy’s intensified focus on its grocery vertical Instamart, the sale of grocery and FMCG products is now its second-largest revenue generator accounting for 20.3% of the operating revenues. These sales ballooned over 3X to Rs 517.4 crore during FY21 from the sales of Rs 168 crore in the previous financial year (FY20).

Importantly, lead generation and sale of groceries are the only two revenue verticals of Swiggy which registered growth during FY20.

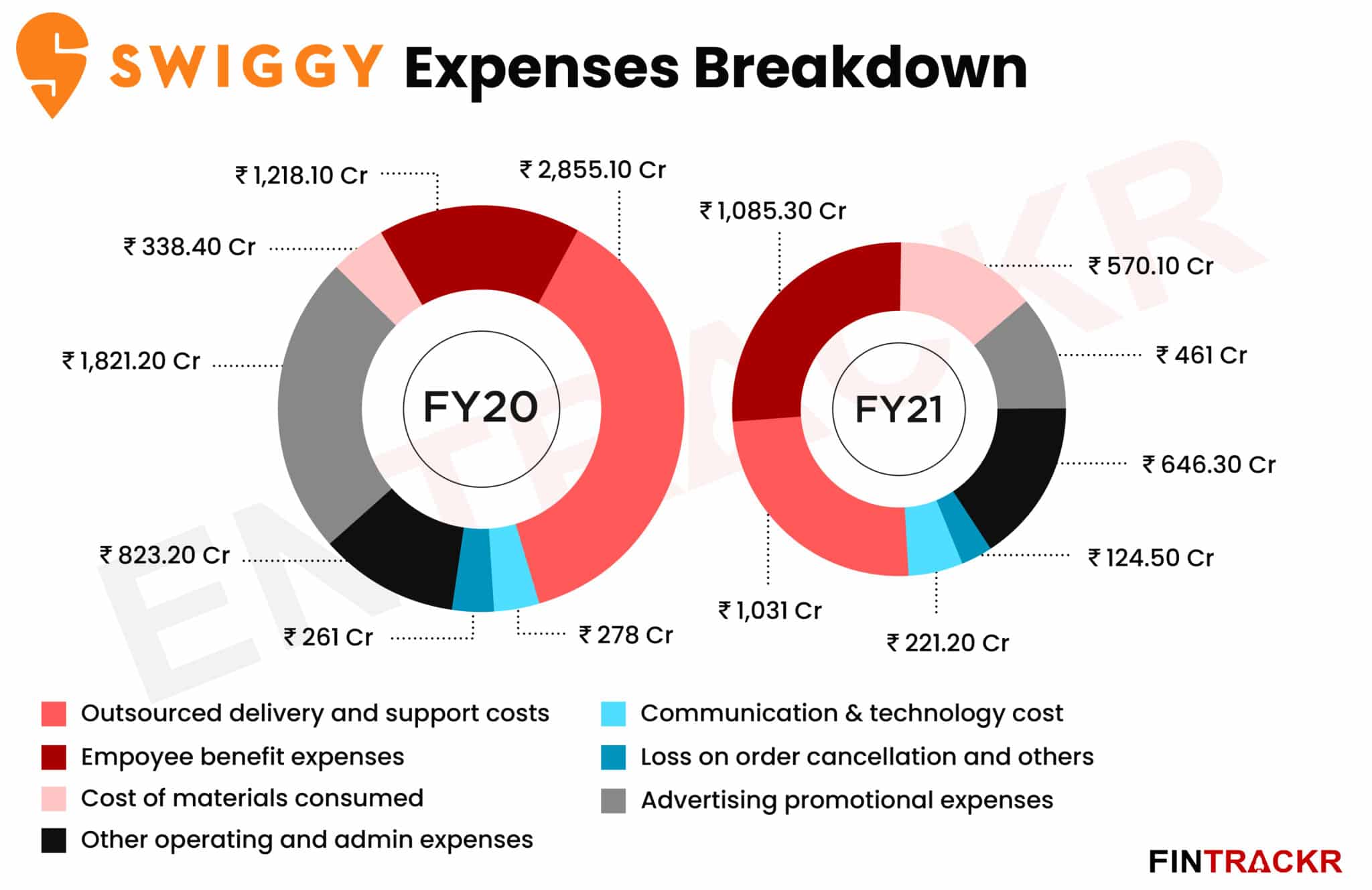

When it comes to expenses, employee benefits expense emerged as the largest cost centre for the company, accounting for 26.2% of the annual costs. Such costs dropped by around 11% to Rs 1,085.3 crore during the last fiscal year (FY21) from Rs 1,218 crore paid out in FY20.

The share of employee stock options (ESOPs) in staff costs has gone up to 20.6% in FY21 from 15.3% in FY20, Swiggy is paying more than one-fifth of staff costs via ESOPs.

The company employs outsourced labour for deliveries and its procurement centres and these costs were reduced by 64% to Rs 1,031 crore in FY21 from Rs 2,855 crore booked in FY20. The main reason for this drop is because the company is recording delivery income after netting off these delivery costs.

The expenses sheet reflects that the management worked towards improving operating margins and austerity measures were put in place to cut back costs where possible. For instance, marketing costs made up nearly 24% of annual costs during FY20 which has now been reduced to only 11% during FY21.

These advertisement and promotional expenses were cut back by 75% to Rs 461 crore during FY21 from Rs 1821 crore spent during FY20.

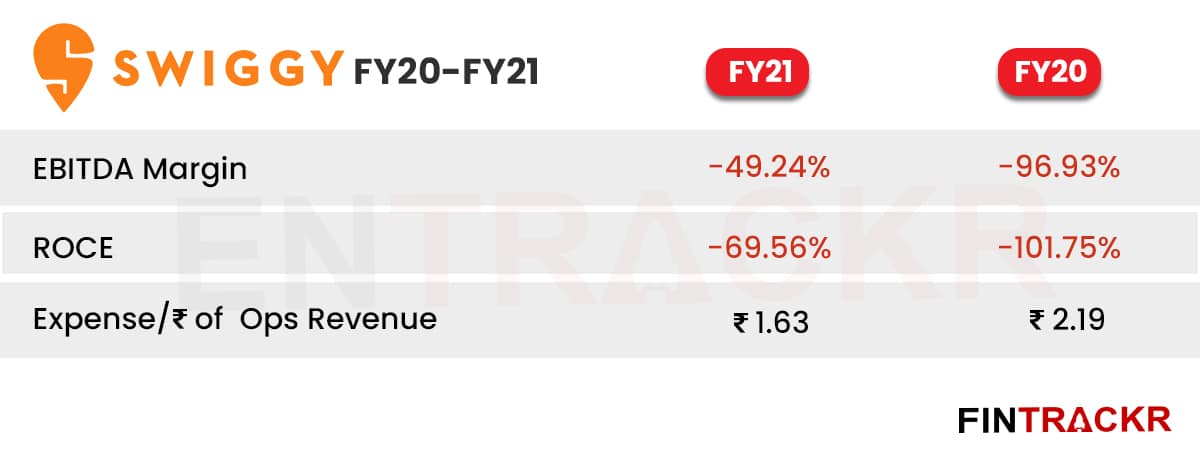

The loss of scale is evident from the 45.5% reduction in annual expenditure, which dropped from Rs 7,595 crore in FY20 to Rs 4,139 crore spent in total during FY21. On a unit level, Swiggy spent Rs 1.63 to earn a single rupee of revenue during the fiscal year ending in March 2021.

With the loss of scale, EBITDA margins have improved to -49.24% in FY21 from -96.93% in FY20. Annual losses have dropped by 58.8% to Rs 1,617 crore in FY21 from Rs 3,920 crore lost during FY20. By the end of March 2021, outstanding losses surged to nearly $1.15 billion or Rs 8,617 crore.

It will be interesting to see how Swiggy keeps improving its margins as the operating scale goes back to pre-covid levels in FY 2021-2022.

It will be interesting to see how Swiggy keeps improving its margins as the operating scale goes back to pre-covid levels in FY 2021-2022.