Trucking logistics firm Rivigo’s B2B express business was taken over by Mahindra in a distress sale in September last year. The company was struggling because of Covid and its failure with the transition to an asset-light model (marketplace one from a full-stack trucking solution).

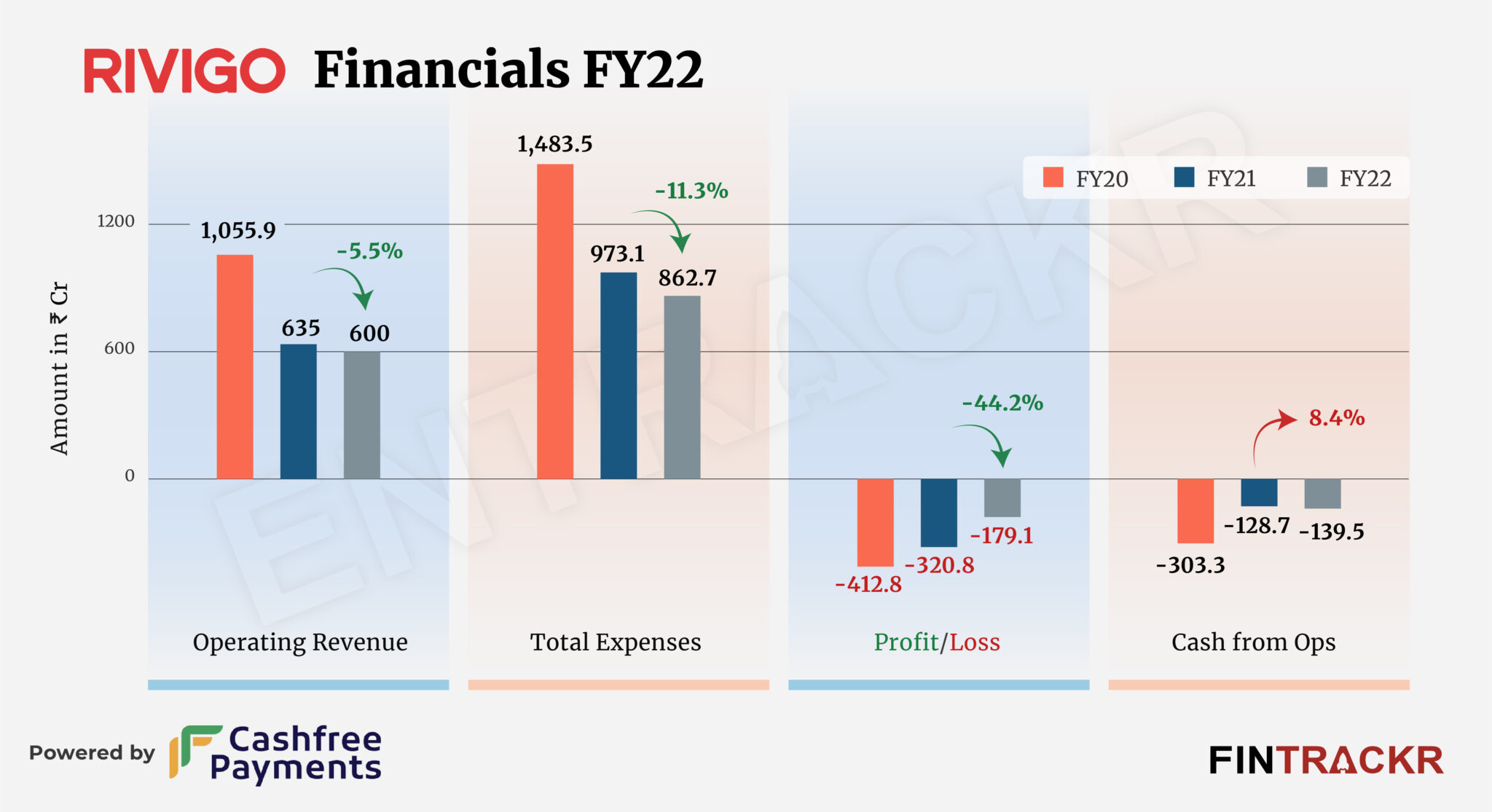

Rivigo’s woes could also be noticed from the erosion of over 40% of its scale in two fiscal years (FY21 and FY22). While the firm’s operating revenue dipped 39.9% in FY21, it slid another 5.5% in FY22.

The company provides trucking facilities across ten industries including apparel, e-commerce, automotive, frozen and processed foods, FMCG, and automotive. The income from these services was the sole source of revenue which decreased 5.5% to Rs 600 crore in FY22 from Rs 635 crore in FY21.

Rivigo also made Rs 83.4 crore during FY22 from the profit on the sale of assets, according to its annual financial statement with the Registrar of Companies.

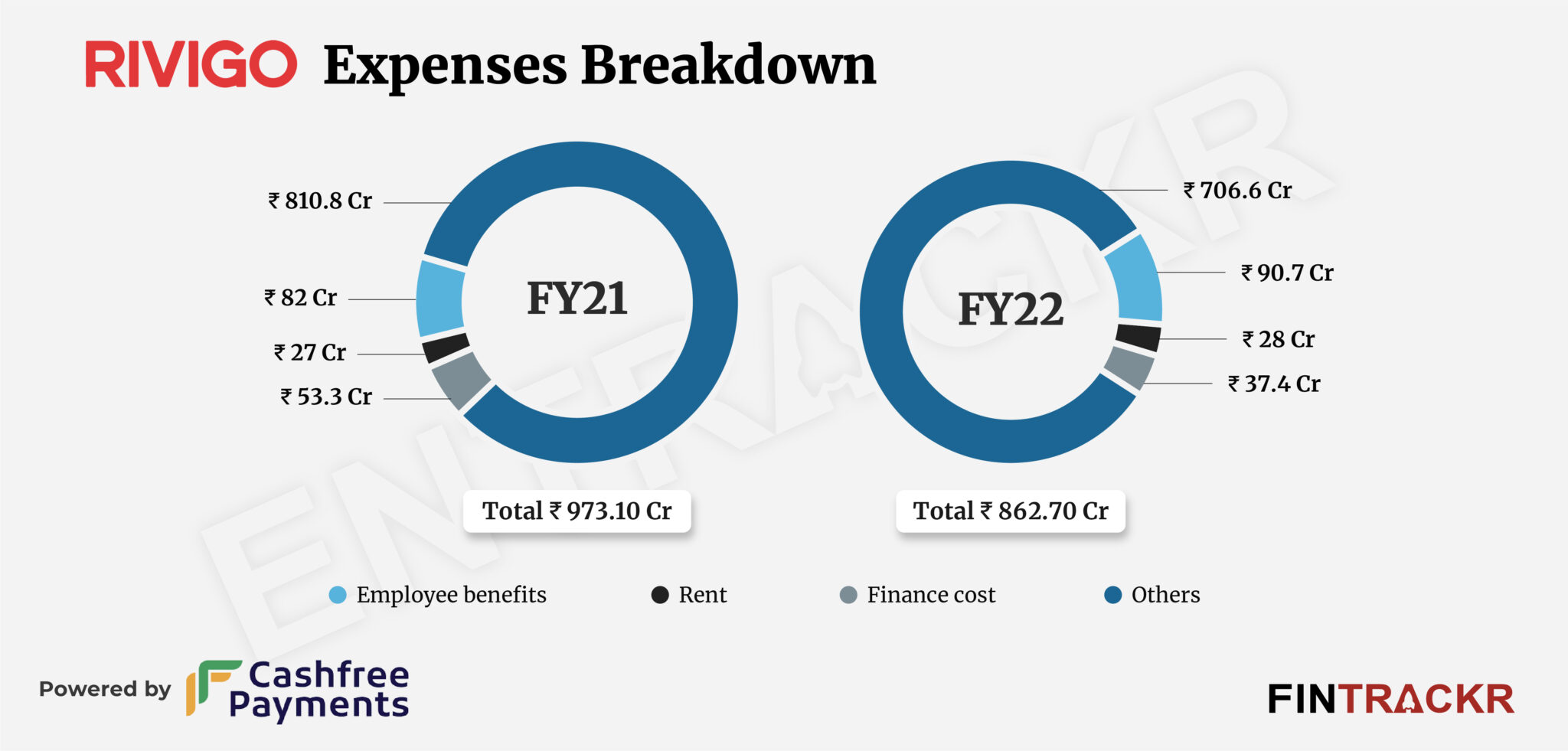

The company didn’t disclose its expense details and booked Rs 556 crore as miscellaneous cost which was 64.4% of the overall expenditure. It covers all trip expenses including fuel, toll, tyre, loading/unloading, and pickup.

Its employee benefit expenses diminished 10.6% to Rs 90.7 crore during FY22 from Rs 82 crore in FY21 while Rivigo’s finance cost also declined 29.8% to Rs 37.4 crore in FY22.

The overall cost for the company narrowed down by 11.3% to Rs 862.7 crore in FY22 from Rs 973.1 crore in FY21. Contraction in the total cost and uneven other income also helped Rivigo to shrink its losses by 44.2% to Rs 179.1 crore in FY22.

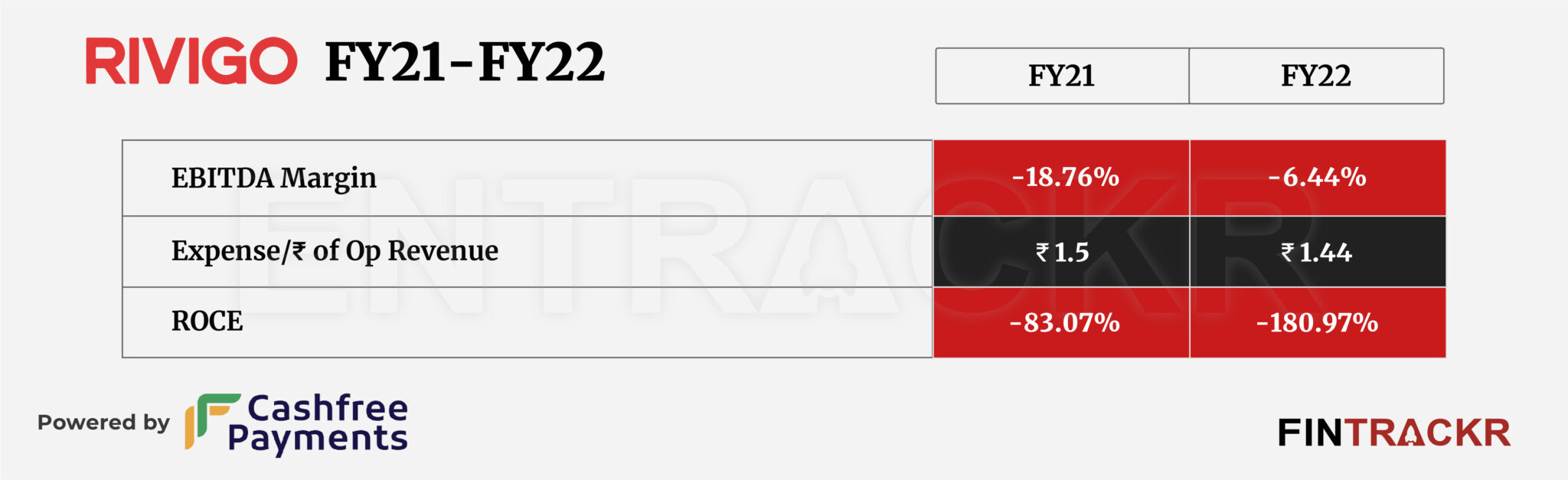

Its ROCE and EBITDA margin stood at -180.7% and -6.44% respectively. On a unit level, Rivigo spent Rs 1.44 to earn a single unit of operating revenue in the fiscal year ending March 2022.

The Mahindra acquisition certainly seems to have paid off on the cost front, as one would expect. However, the challenge now would be to grow again, as the same advantages of being part of a larger industrial group in terms of financial discipline can hurt when it comes to moving like a startup to grab growth opportunities.

Be it talent, financing or deals, Rivigo will be an interesting study when its FY23 numbers finally come out, to offer clarity in terms of the plans of the new owners for it. In such cases, selling the unit off can never be put off the table if the buyer decides that long term integration, culturally and functionally will actually be counter productive. Especially when a ready market with buyers for the business is available again by then.