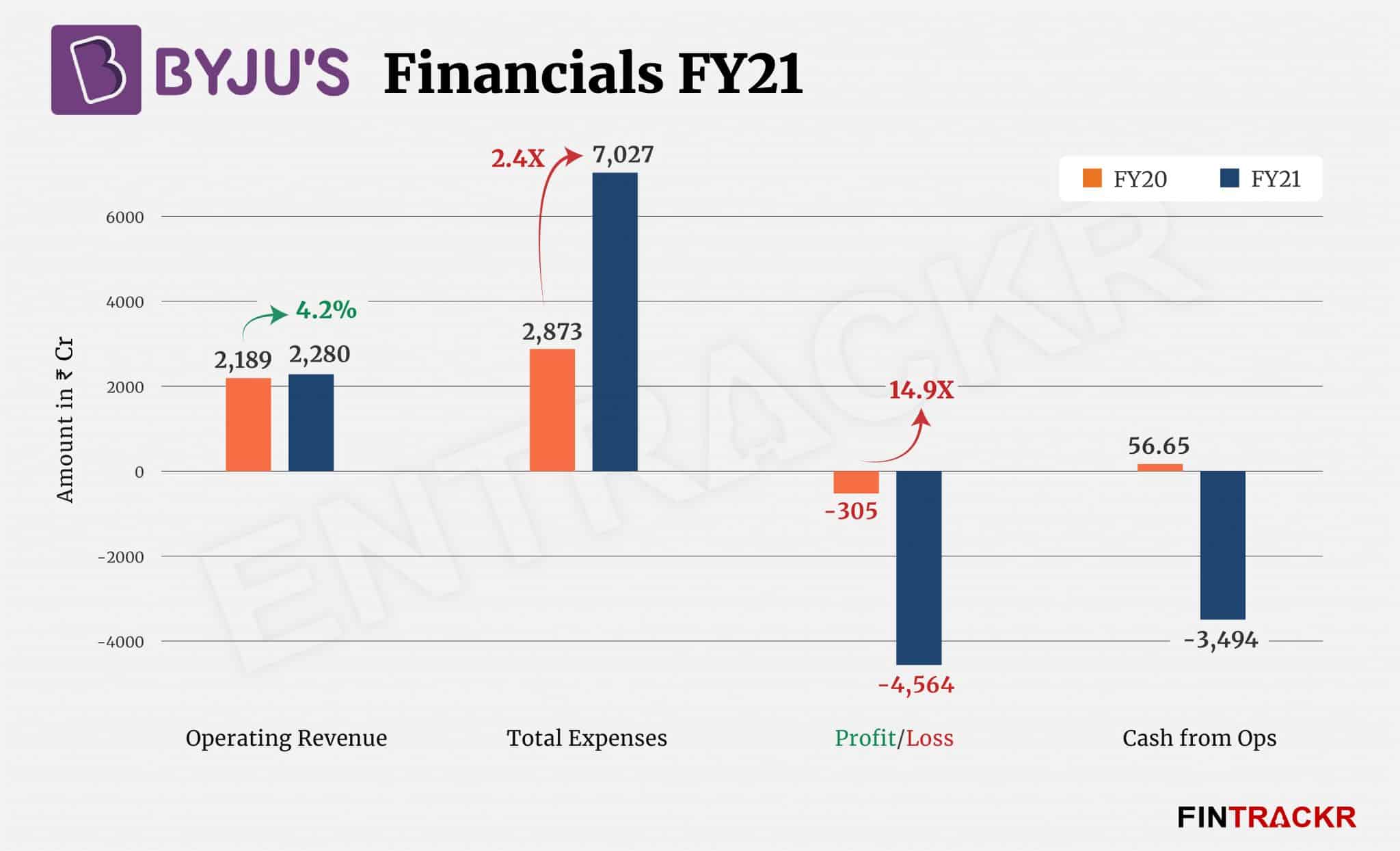

The wait is finally over and Byju’s has filed its detailed annual financial statement for the fiscal year ending March 2021 with the Registrar of Companies (RoC). And it does make for some strange reading for the lay observer. In a year when edtech firms boomed thanks to the pandemic and its enforced online shift, Byju’s revenue from operations barely grew 4% to Rs 2280 crore in FY21 from Rs 2,189 crore in the previous fiscal year (FY20).

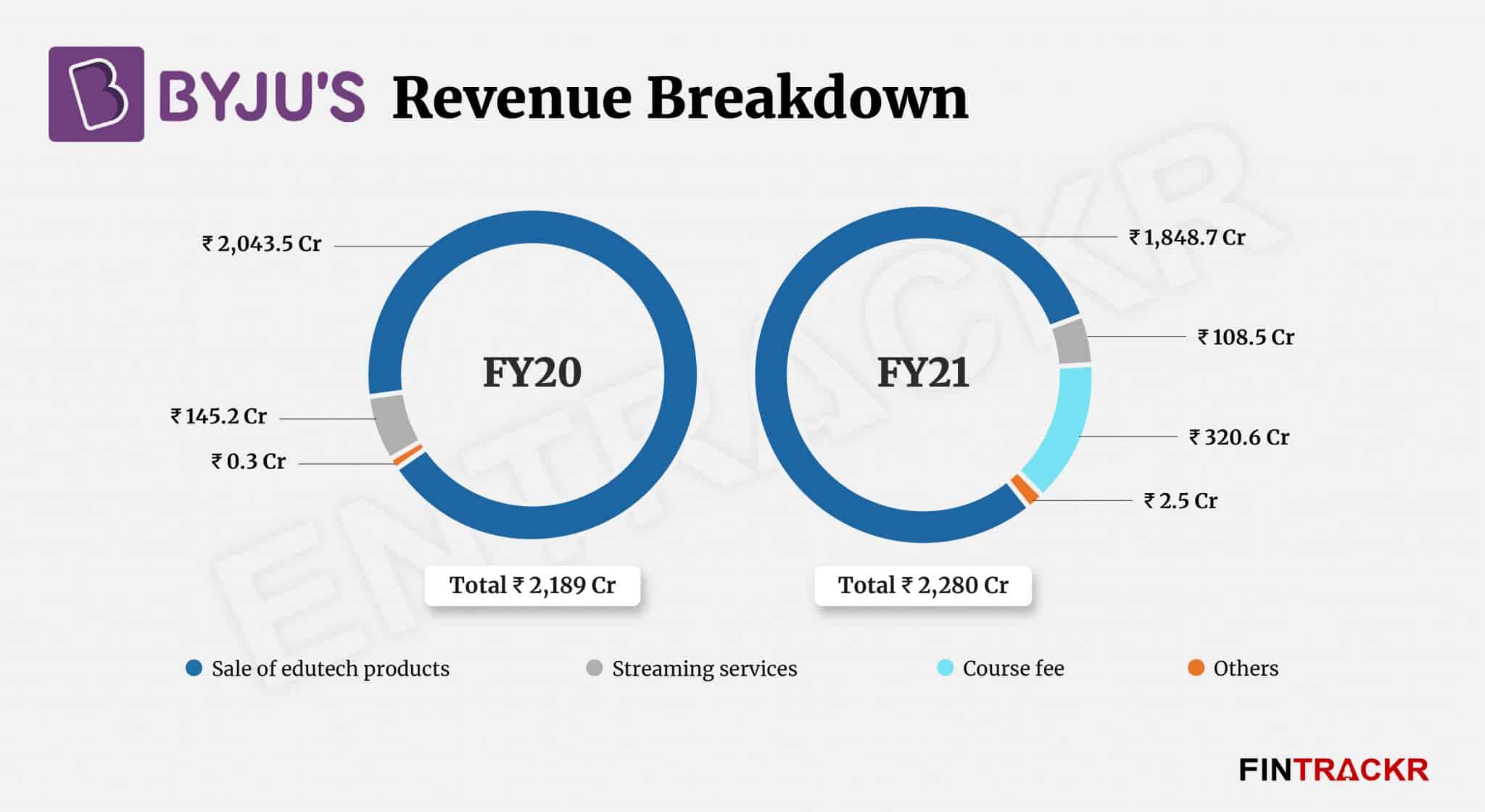

However, the company’s losses ballooned 14.9X to Rs 4,564 crore during the same period. We will come later on the expense and loss patterns of the company. For now, let’s focus on its revenue generation channels. The sale of edutech products which include tablets, SD cards, tech-enabled devices and laptops constitute 81% of Byju’s revenue in FY21. Collection from this vertical reduced by 9.5% to Rs 1,848.7 crore during the same period.

Course fees and streaming were other sources of revenue for the edtech giant which collectively stood at Rs 429 crore in FY21.

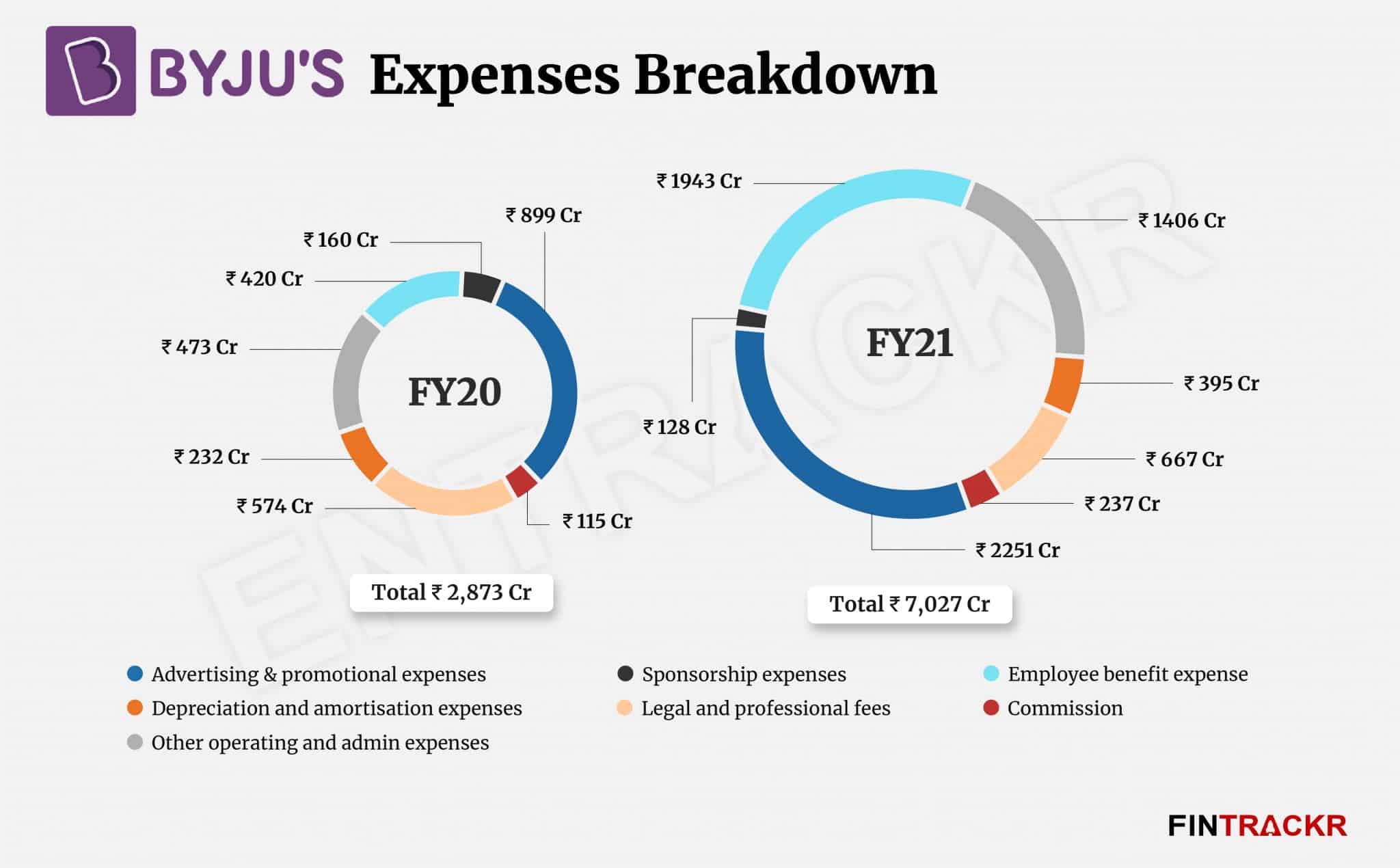

On the expenses front, advertisement and promotion expenses were the largest cost center for the company forming 32% of the overall expenses. This cost surged 2.5X to Rs 2,251 crore in FY21.

Employee benefit expenses were the second largest expense for Byju’s which shot up 4.6X to Rs 1,943 crore in FY21. This also includes Rs 476 crore as ESOP expenses, which were settled in equity.

The company has to pay a commission to the parties for the sale of educational content to customers based in the Gulf Cooperation Council (GCC) countries. Byju’s booked a commission expense of Rs 237 crore in FY21 on the sale of Rs 497 crore to GCC countries in FY21.

Legal and professional fees grew 16% to Rs 667 crore in FY21 whereas the company added another Rs 128 crore as sponsorship expenses. The expenditure on compliances were apparent as Byju’s had acquired several companies in FY21. At the end, the company’s total expenses blew up 2.4X to Rs 7,027 crore in FY21.

Importantly, Byju’s wrote off around Rs 816 crore as the cost of intangible assets under development from the overall cost. If the company includes this cost, its expenses would have spiked to Rs 7,843 crore in FY21.

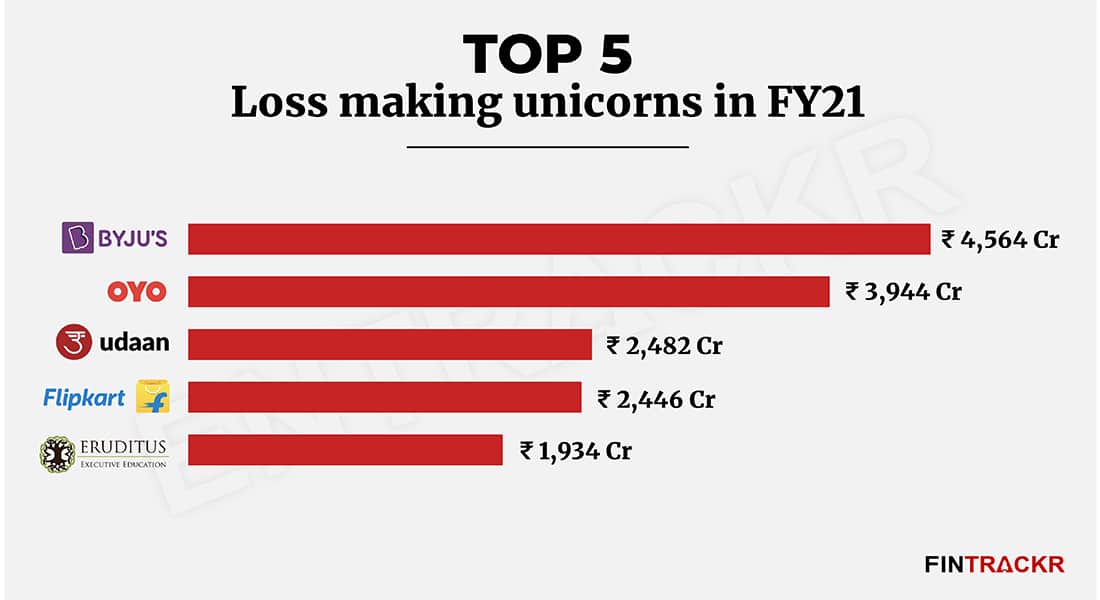

With such a huge expense sheet, losses of India’s most valued edtech startup rocketed 14.9X to Rs 4,564 crore in FY21. Counting the amount it has written off as capital expenditure, the losses would have crossed Rs 5,380 crore for FY21.

Byju’s is also on top in terms of losses among all unicorns including Flipkart in FY21.

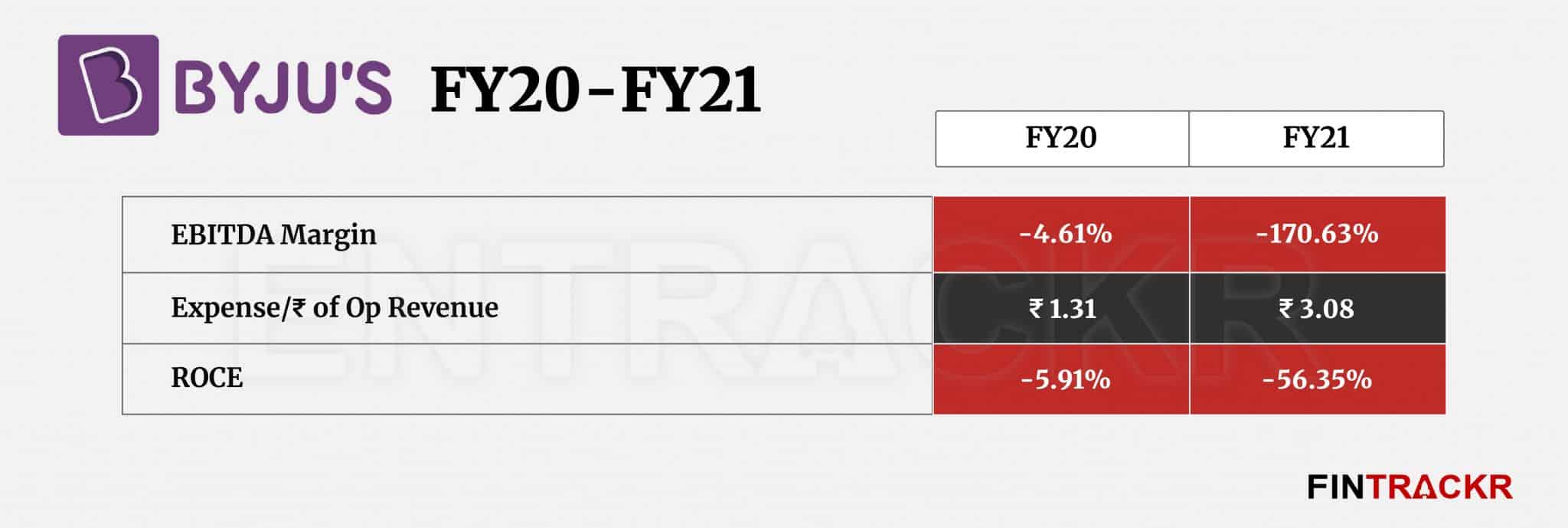

On a unit level, Byju’s has spent Rs 3.08 to earn a single unit of operating revenue. The huge gap between cost and revenue worsened the EBITDA margin and ROCE of the company to -170.63% and -56.35% respectively in FY21.

Byju’s also made three acquisitions during FY21: WhiteHat Jr, Scholr and Aristotle. While it acquired 76% shares of Whitehat Jr in all cash-deal of Rs 1,327 crore, Inspilearn Education (Scholr) and Digital Aristotle (Aristotle) were acquired for Rs 20 crore and Rs 16.5 crore respectively.

Byju’s numbers, coming as they did after a protracted delay of 18 months, only created grounds for multiple theories. And are disappointing by any stretch, no doubt. One would argue that the detailed breakup gives no sign that a significant turnaround is imminent.

That explains why founder Byju Raveendran opened up to the media after the preliminary results came out, to try and remove the clouds of doubt over the firm’s prospects. Like blaming the growth stagnation on the change in revenue recognition accounting in FY21, as well as the recognition of EMI driven sales only after significant collections were made.

In retrospect, both seem very obvious and needed changes, and are unlikely to reassure investors. While the anecdotal chatter around its business practices can still be ignored if you give it credit for its size and scale, Byju’s claim of being done with layoffs has already fallen flat after news floated out of a further offloading of 2,500 employees (out of a workforce size of around 50,000) last week, due to what has been termed growth fears in most reports.

Raveendran’s claims of turning in a strong performance post FY21 might yet show up in the topline for FY22, but if FY23 is already looking weak, you have to wonder if the current model is sustainable, or capable of generating the kind of returns investors have paid for.