Earlier this month, consumer lending platform Kissht raised $80 million in its largest institutional funding round led by Vertex Growth and Brunei Investment Agency. The firm raised the Series E round at a valuation of $500 million and will be using it to scale book size and technology backend.

The company was also looking to foray into the BNPL cards segment directly in competition with the likes of Slice and Uni but the Reserve Bank of India’s latest crackdown is likely to derail its pay later ambition.

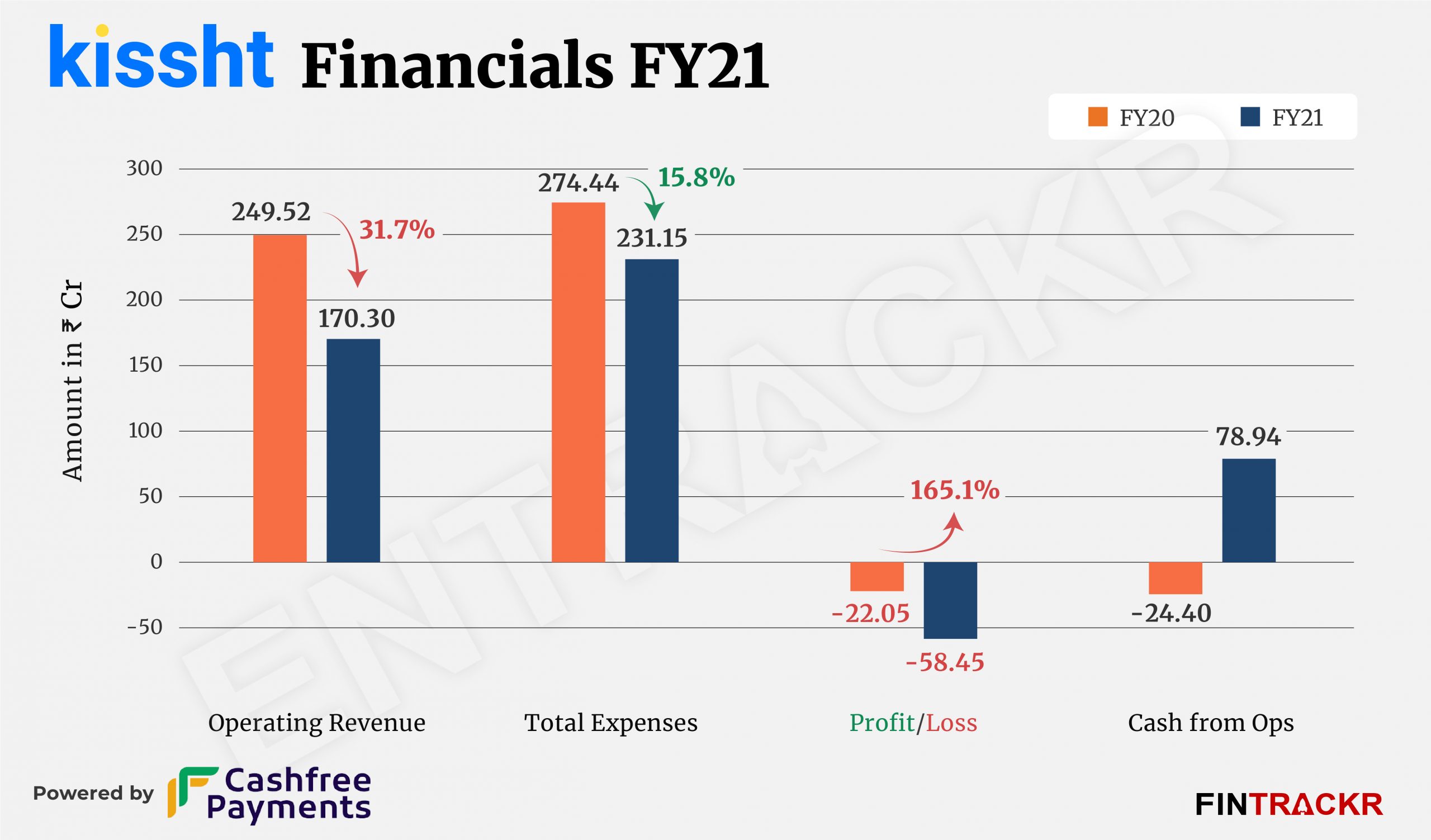

While the future of Kissht’s BNPL card appears hazy, let’s take a look at the company’s growth during the last reporting period (FY21). The six-year-old firm saw its revenue from operations contract by 31.7% to Rs 170.3 crore during FY21 from Rs 249.5 crore in FY20.

The company claims to have partnered with more than 500 online and over 3K offline partners including Amazon, Samsung & Vijay Sales. Kissht uses its proprietary software algorithm, and credit marketplace platform to provide loans to users.

Going over the multiple revenue streams, we observed that the company generates 50.8% of its revenues in the form of processing fees collected at the time of the release of loans. Processing fees is Kissht’s largest revenue driver, growing by 21.4% to Rs 86.5 crore in FY21 from Rs 71.2 crore in FY20.

Meanwhile, earnings from interest on loans has dropped by 60.5% to Rs 48 crore in FY21 from Rs 121.62 crore earned during the previous fiscal (FY20).

The Mumbai-based company earned another Rs 35.84 crore from the provision of other ancillary services during the fiscal ended in March 2021.

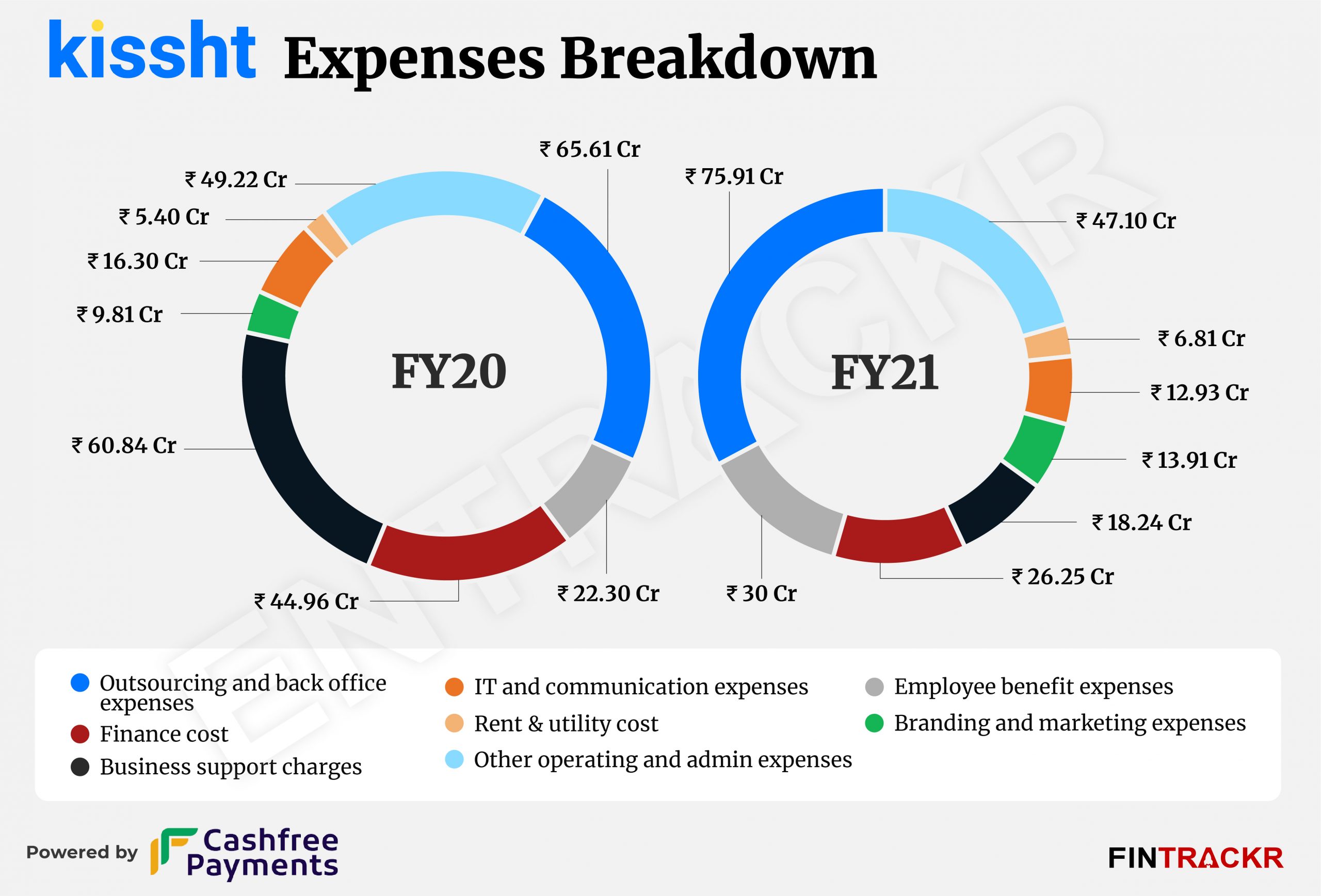

Moving over to the expense sheet, back office and business support costs stood out as the largest cost centre for the company accounting for 40.7% of its annual expenditure. As the volume of loans dropped, these costs dropped by 26% to Rs 94.2 crore in FY21 from Rs 126.5 crore during FY20. On similar lines, finance costs were also reduced by 41.6% YoY to Rs 26.3 crore in FY21.

Employee benefits payment was the second largest cost for Kissht, making up 13% of its total expenditure and growing by 34.5% YoY to Rs 30 crore during FY21. Moreover, Kissht’s expenditure on advertising and marketing surged by nearly 41.8% to around Rs 14 crore while rent and utility payments grew by 26% YoY to Rs 6.8 crore during FY2020-21.

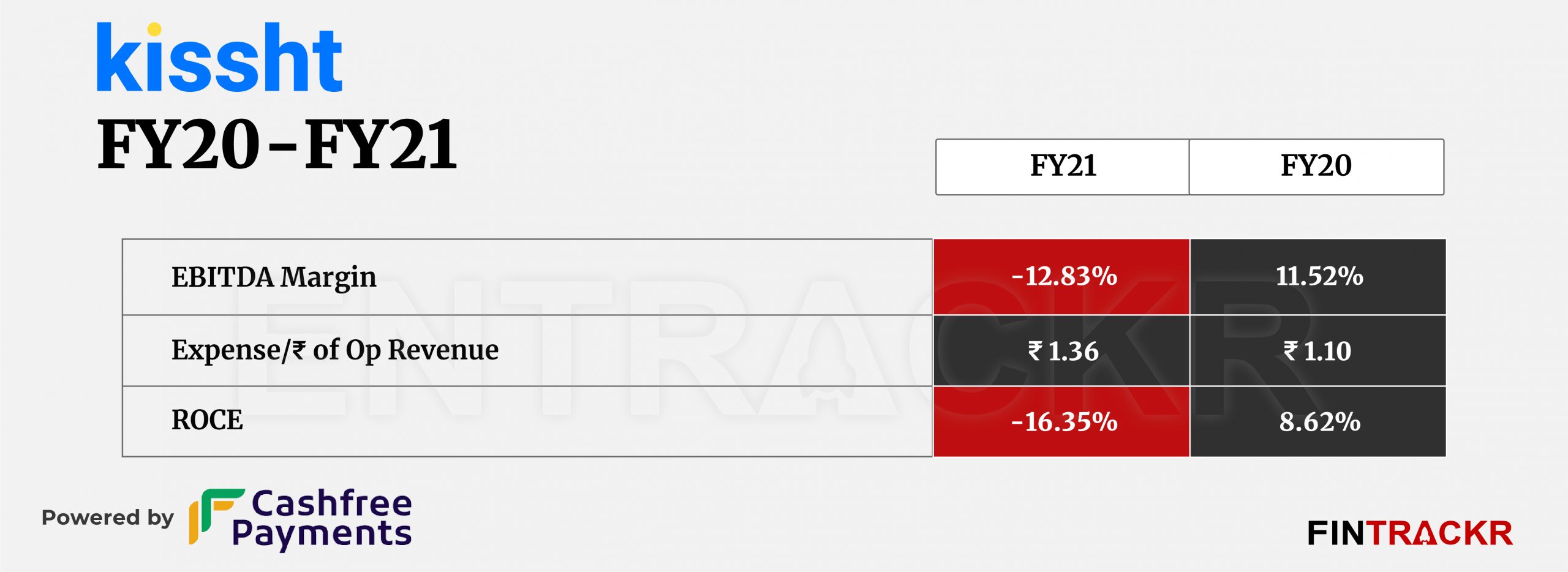

IT and communications costs of Rs 12.93 crore pushed annual expenditure to Rs 231.2 crore in FY21 which dropped by 15.8% as compared to Rs 274.4 crore spent in total during FY20. Kissht spent Rs 1.36 to earn a single rupee of operating revenue during FY2020-21.

The fiscal affected by COVID 19 disruptions was challenging for Kissht as consumer demand contracted and the company suffered problems of unpaid loans. It booked bad debts worth Rs 23.4 crore during the last reported financial year due to non-repayments of loans.

The reduction in revenue along with NPA resulted in heavy losses for the company which surged by 165.1% to Rs 58.5 crore in FY21 as compared to Rs 22.05 crore it lost during FY20.

While the company is yet to file financial statements for the fiscal year ending March 2022, Kissht claimed a 2.4X jump in its revenue in FY22. According to the firm, its total consolidated revenue stood at Rs 410 crore during the last fiscal year with Rs 55 crore profit (before tax). While those numbers and the recent funding round would seem to vindicate those claims, the fact remains that the RBI’s move on limiting credit card loans to banks will be a setback for the firm too. Delivering a strong FY23-24 performance will be a test of agility and adaptability, as much as the highly competitive marketplace it already is, with no dearth of other funded startups in the space.