Online pharmacy platform PharmEasy has filed its draft red herring prospectus (DRHP) to raise Rs 6,250 crore in its upcoming IPO. API Holdings Limited, the holding entity for the PharmEasy group which controls 26 subsidiaries including Aknamed, Docon, Retailio and Thyrocare will also raise Rs 1,250 crore via private placement in a pre-IPO round.

Importantly, the planned IPO breaks from the recent trend of ‘new age’ firms with exclusive issues of new shares and zero secondary sales by existing holders.

As per the DRHP, PharmEasy will utilise Rs 1,929 crore for prepayment or repayment of all or a portion of certain outstanding borrowings availed by the company. Further, it will utilize Rs 1,259 crore to fund organic growth initiatives including marketing and promotional activities, improvement of supply chain and ramp up technology infrastructure.

Another Rs 1,500 crore will be used for pursuing inorganic growth through acquisitions and other strategic initiatives and the rest for general corporate purposes.

The Mumbai-based company has acquired five major health and pharma companies during FY20-FY21 till now which include Ascent Healthcare, Thyrocare, Aknamed, Marg ERP and Medlife International. These strategic acquisitions have helped the company to increase its scale of operation vastly from technology Solutions, Pharma distribution and Diagnostics solutions.

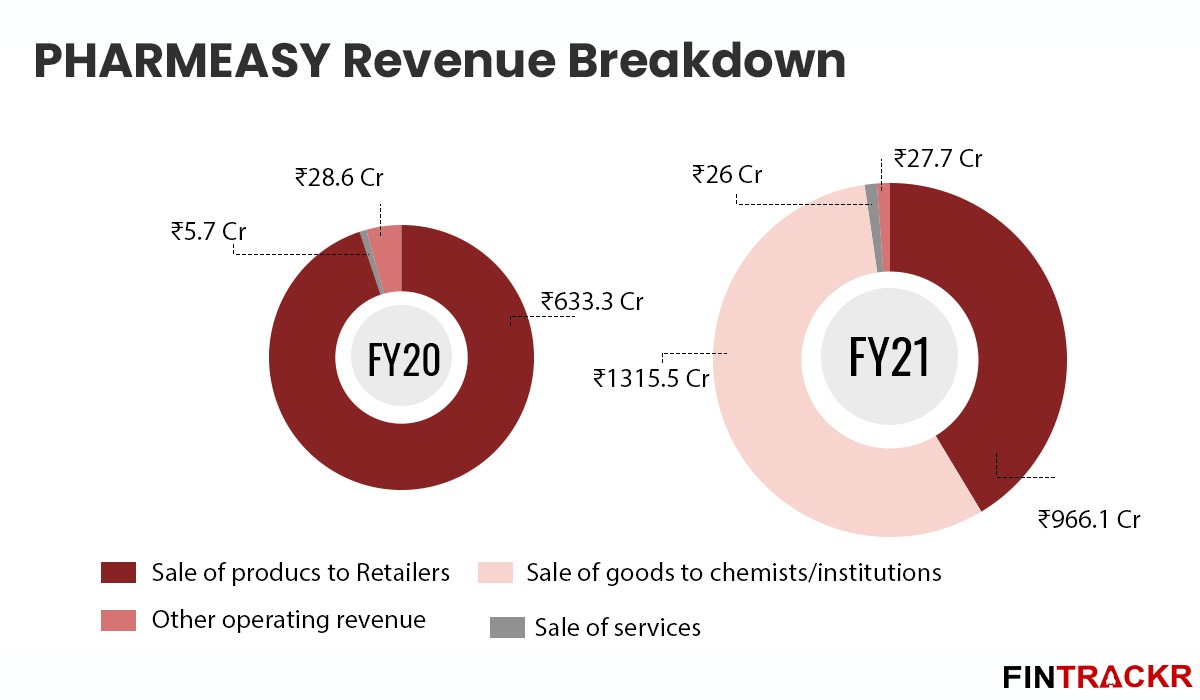

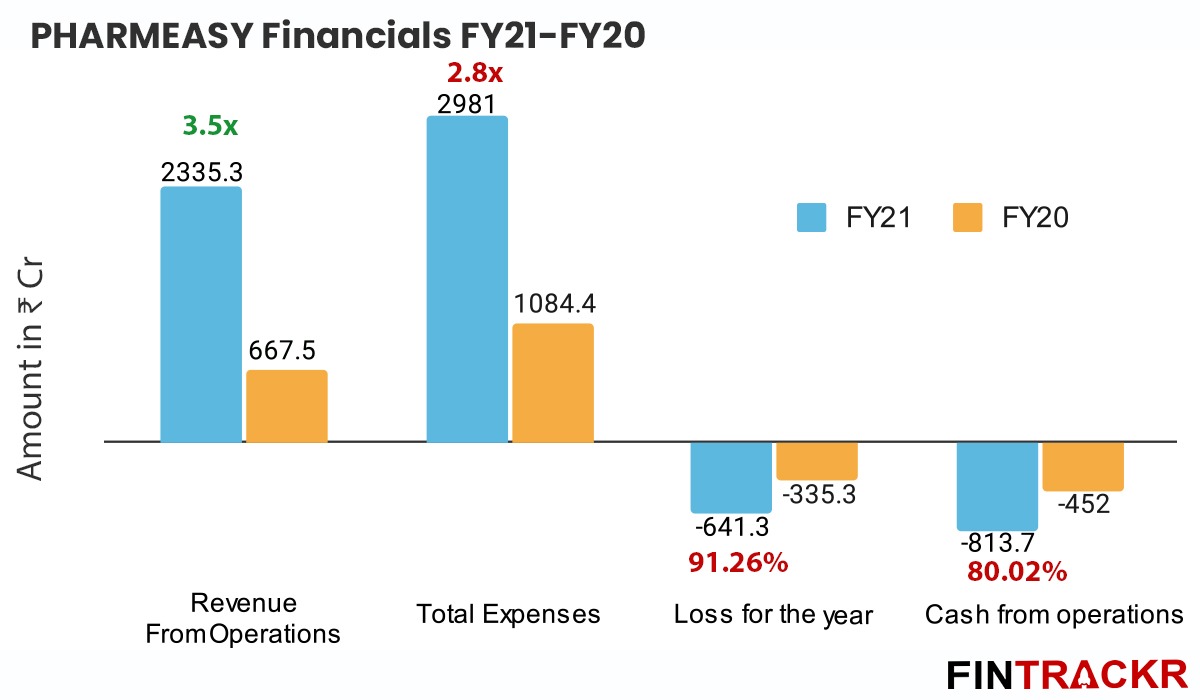

The increase of scale is evident in the operating revenue of the business which went up 3.5X to Rs 2,335.3 crore in FY21 from Rs 667.5 crore in FY20. PharmEasy also benefited from the sale of medicines from its online platform during the Covid-induced lockdowns. Its distributional channel business to supply medicine and wellness products to chemists and institutions (hospitals & dispensaries) stood out as the largest revenue vertical for the company.

PharmEasy collected Rs 1,315.5 crore from the distribution channel business which accounted for 56.3% of its revenue in FY21 whereas this vertical was non-existent during FY20.

Retail sale of products brought in Rs 966.1 crore while the provision of diagnostics, direct to pharmacy service and technology fulfilment services collected Rs 26 crore for the company during FY21. PharmEasy also collected other operating income of Rs 27.7 crore and finance income of Rs 25.4 crore during the fiscal ended in March 2021.

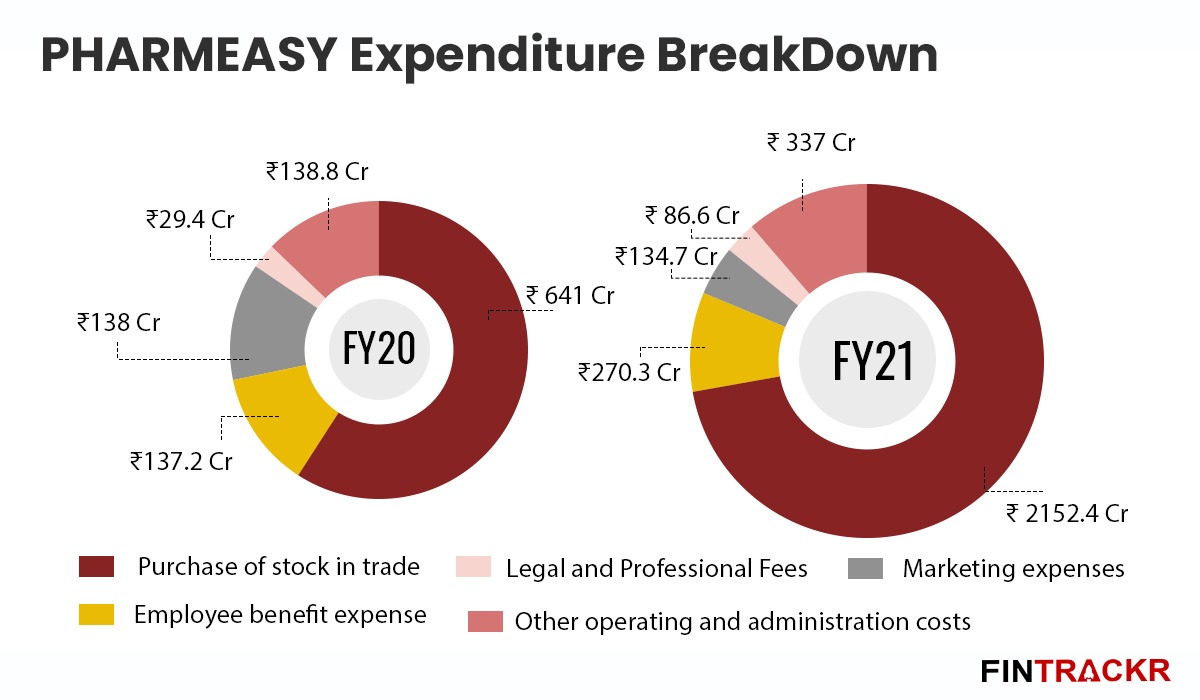

When it comes to expenses, the cost of procuring the stock in trade was the biggest one for the company, accounting for 72.2% of annual expenditure. These costs grew in line with revenues and GMV after the acquisitions of Ascent and Medlife, increasing 3.4X to Rs 2,152.4 crore in FY21 from Rs 641 crore in FY20.

PharmEasy’s employee base eventually grew after several acquisitions and the increase of scale and payments of employee benefits grew by 97% to Rs 270.3 crore in FY21 from Rs 137.2 crore in FY20. Significantly, sales promotion and marketing expenses remained relatively flat, amounting to Rs 135 crore during FY21.

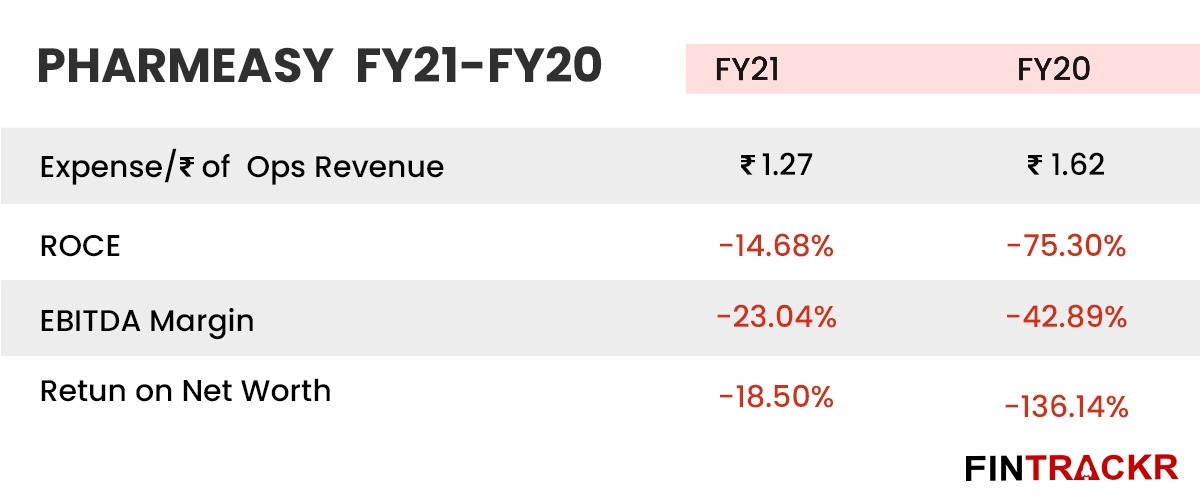

PharmEasy’s annual costs surged 2.8X to Rs 2,981 crore in FY21 from Rs 1,084.4 crore in FY20. On a unit level, it spent Rs 1.27 to earn a single rupee of revenue, improving by 22% from Rs 1.62 spent for the same during FY20.

PharmEasy’s annual costs surged 2.8X to Rs 2,981 crore in FY21 from Rs 1,084.4 crore in FY20. On a unit level, it spent Rs 1.27 to earn a single rupee of revenue, improving by 22% from Rs 1.62 spent for the same during FY20.

Prima facie, it seems that the company burned more cash during the last fiscal as annual losses spiked by 91.3% to Rs 641.3 crore in FY21 from Rs 335.3 crore in FY20. But its EBITDA margin improved vastly from nearly -43% in FY20 to -23.04% in FY21 even after increasing its operating scale more than three folds.

Importantly the FY21 numbers quoted above do not include the earnings of listed diagnostics giant Thyrocare which was acquired by PharmEasy in June this year. It controls 71.22% stake in the diagnostics company after payment of Rs 4,895.3 crore as purchase consideration. Thyrocare’s Q1FY22 results indicated revenues of Rs 164.6 crore, reaping profits of Rs 75.3 crore during the period.

As part of the DRHP, PharmEasy has also submitted its quarterly results for Q1 FY22 recording operating revenue of Rs 1,197 crore for the three month period at an annual run rate of Rs 4,788 crore. It spent Rs 1527 crore during the first quarter, losing nearly Rs 314 crore. The company had last raised $217 million in a pre-IPO round last month at a post-money valuation of $5.7 billion. It raised the private placement round at a revenue multiple of 17X considering last fiscal earnings.

Much like many of the recent string of IPO’s from digital-first firms across sectors, PharmEasy also has few comparable listed peers, and that makes its eventual market valuation difficult to estimate. The market has stumped most people with the high valuations given to both Zomato, and now Nykaa, even after what was considered aggressive pricing. On the other hand, Paytm’s IPO scraped through without any significant participation from a category like mutual funds, indicating continuing evolution of perceptions and risk appetite among institutional buyers.

At least in the healthcare sector that PharmEasy straddles, we have listed firms across the different segments it has a presence in. So it will all come down to the premium it seeks for the digital strengths it has, as the underlying businesses are well understood. Whether that leads to a moderate pitch on valuations or learning from the examples cited above, an even more aggressive pitch, remains to be seen.