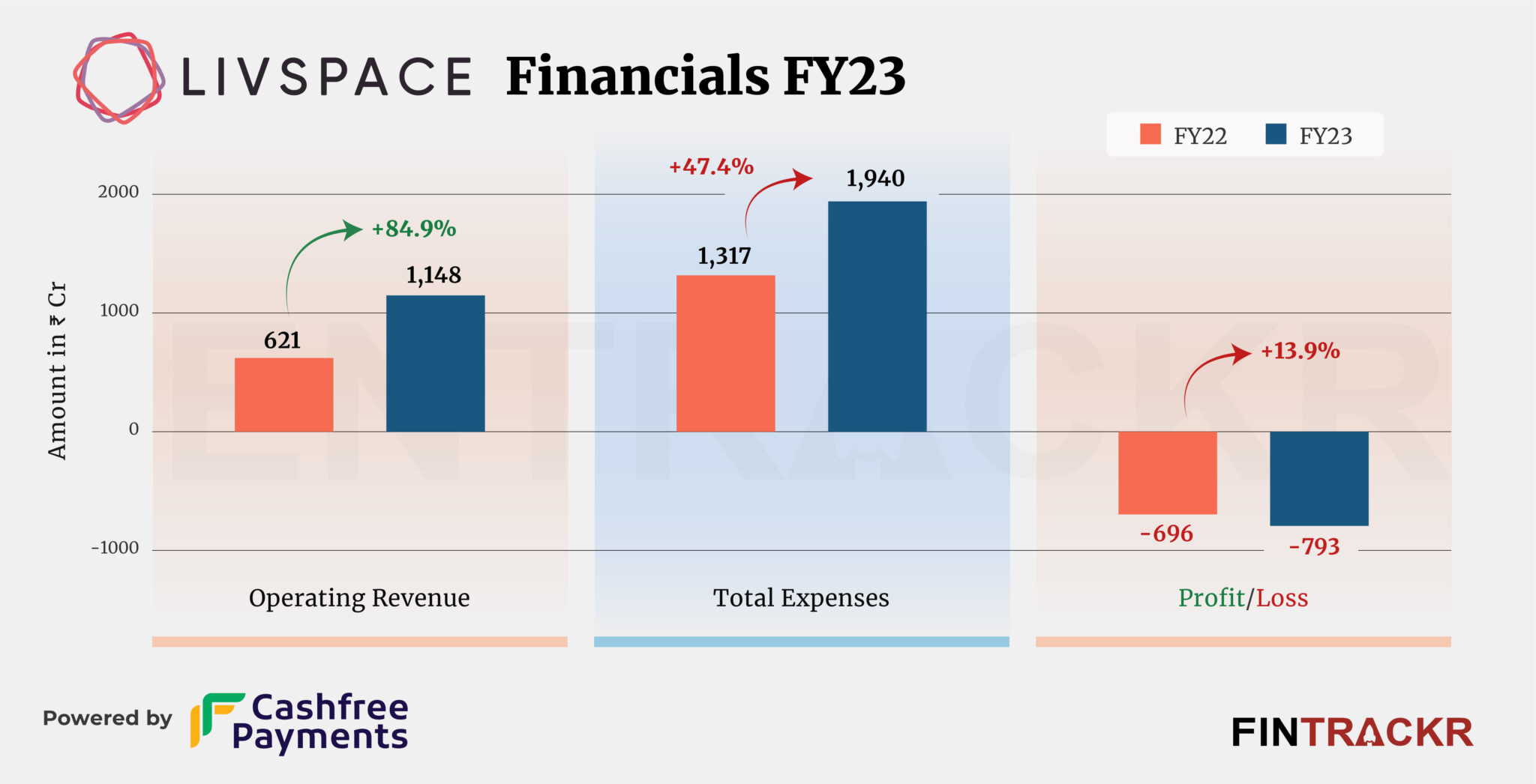

Omnichannel home interior and renovation platform Livspace grew at a rapid clip with 85% year-on-year growth during FY23. But the KKR-backed firm posted a loss of nearly Rs 621 crore (SGD 101.7 million) during the same period.

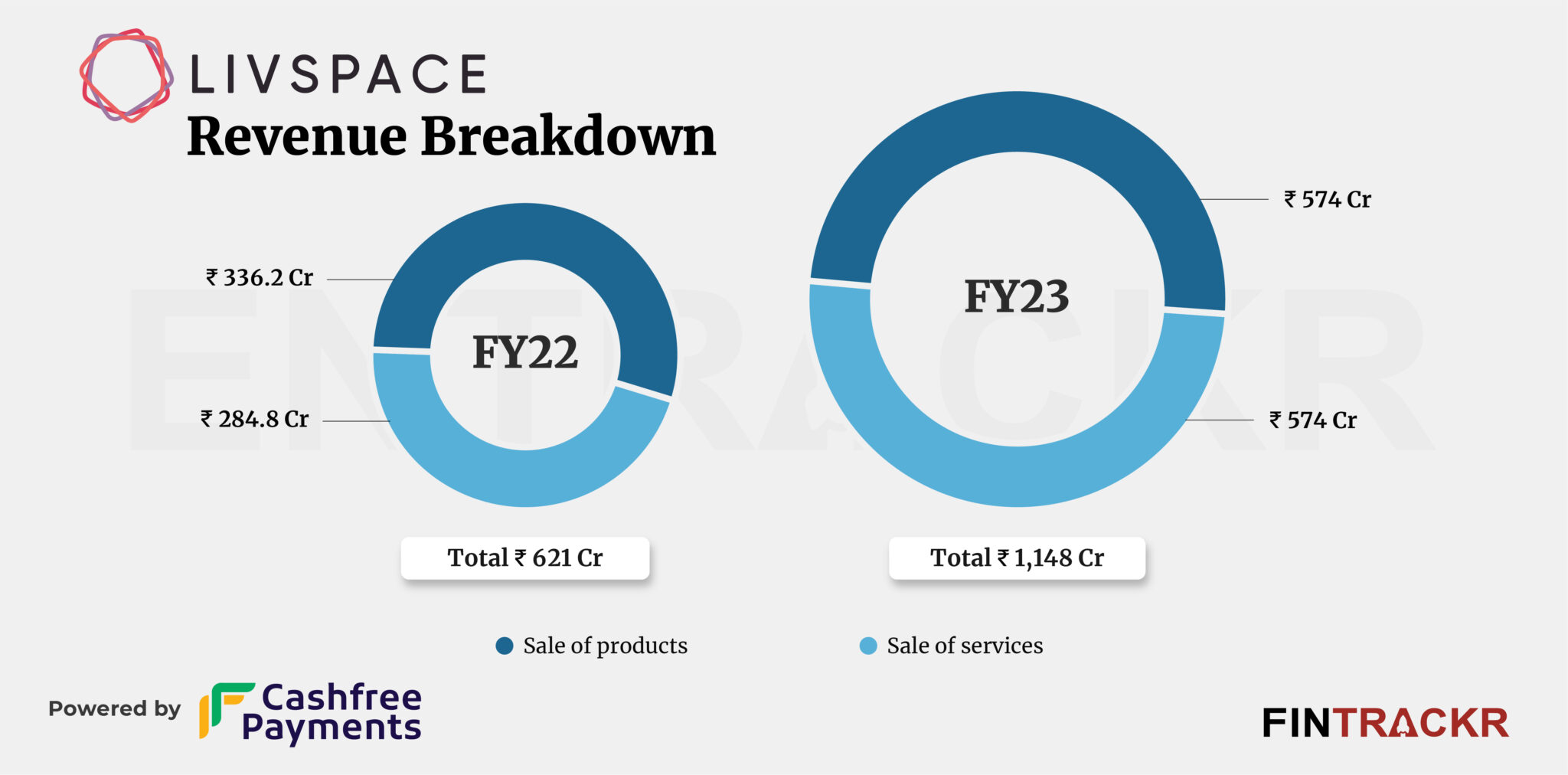

Livspace’s revenue from operations surged to Rs 1,148 crore (SGD 188.1 million) during FY23 from Rs 621 crore (SGD 101.7 million) in FY22, according to its consolidated annual financial statements filed by the group company in Singapore.

Livspace allows homeowners to discover pre-designed rooms, kitchens, and storage areas on its platform. The sale of products accounted for 50% of revenue which surged 70.5% to Rs 574 crore FY23. The company also provides a marketplace for interior services to residential customers and related vendors. With over 3,500 designers, income from this segment soared 2.2-fold to Rs 574 crore during the previous fiscal year.

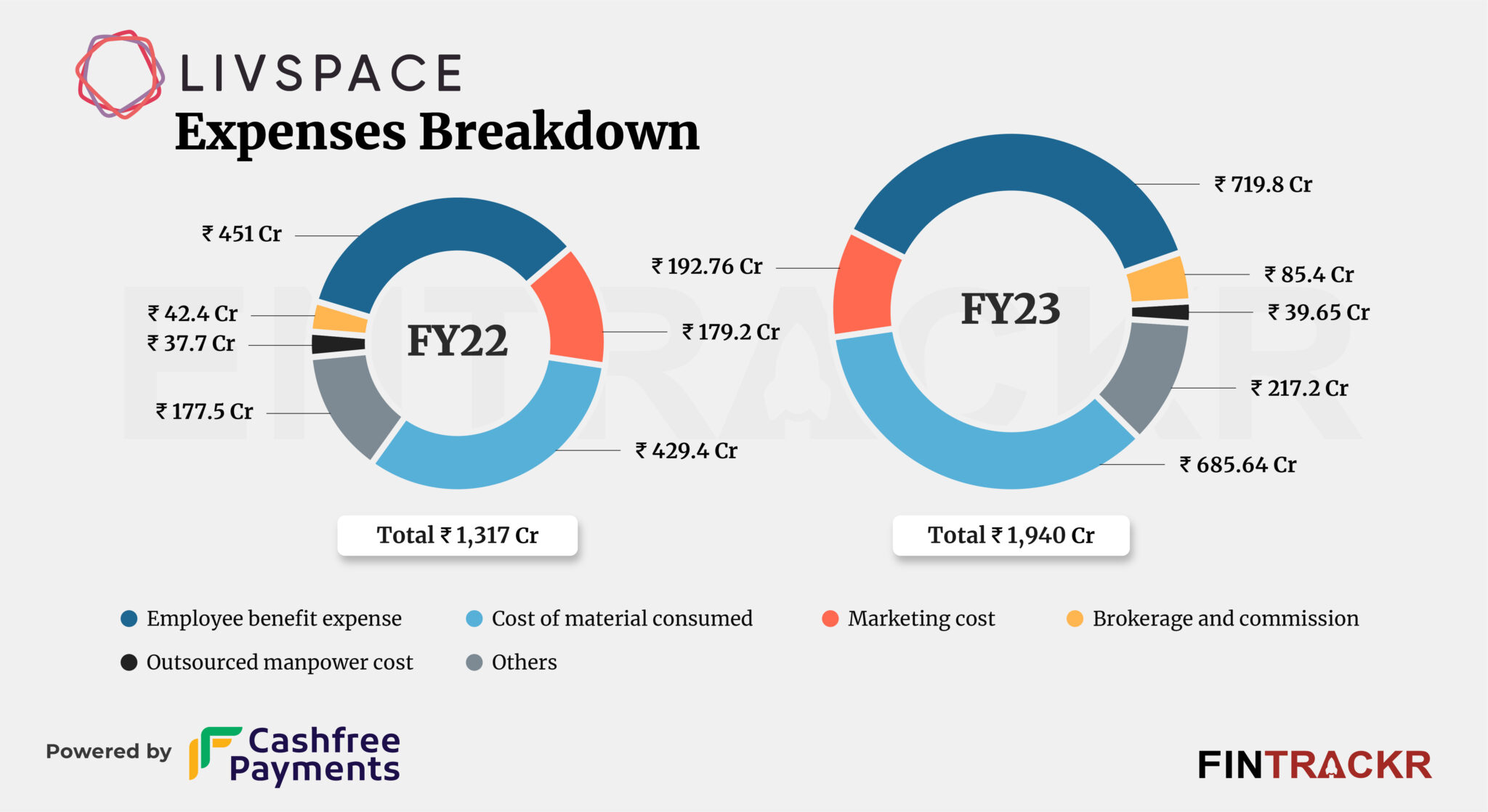

On the cost side, employee benefits formed 37.1% of the overall expenditure which surged 59.5% to Rs 719.8 crore during FY23. This includes Rs 170 crore as ESOP cost (non-cash).

The cost of material consumed was the second largest cost center for Livspace. In the line of scale, this cost rose by 59.7% to Rs 685.64 crore during FY23. The company added another Rs 192.6 crore and Rs 85.4 crore towards marketing costs and brokerage and commission which pushed Livspace’s overall expenditure by 47.4% to Rs 1940 crore in FY23.

It’s worth noting that we have ignored the cost of Rs 414 crore (SGD 68 million) against impairment of financial loss (an adjustment of accounting standards) during FY22.

The company’s noticeable growth and effective management of expenses played a significant role in mitigating its losses, which increased by a mere 13.9% to Rs 793 crore in FY23. Importantly, Livspace’s total outstanding losses stood at Rs 5,160 crore (SGD 846 million) during FY23.

Its ROCE and EBITDA stood at -88.63% and -61.62% during FY23. On a unit level, the company spent Rs 1.68 to earn a unit of operating revenue.

While wiping out accumulated losses might be some time away, operating breakeven doesn’t seem so distant for the home interior platform. A strong market in India promises to take care of that, even though the usual issues of a large unorganised sector and intense margin pressure will continue to challenge it like other organised players in the category.

Players in the segment really need a breakthrough marketing move that helps them stand out from the clutter, and build a sustained pipeline of business around a strong brand. For whatever reason, we haven’t seen that yet in India, in our view. Promises like a 10-year warranty are either not credible or haven’t been communicated strongly enough, despite the high marketing costs. But like its investors, we would bet on the firms finding a way, and Livspace, having done the hard miles by coming this far, should certainly be ahead in that race.

Note: In order to maintain consistency within the company, we have adopted a fixed exchange rate of Rs 61 for the Singapore dollar during the analysis of financial statements for FY23 and FY22.