“Raising collateral-based or term loans without profitability is like playing with fire,” said a unicorn founder, who also runs an early-stage fund.

The extreme caution — akin to the danger sign on an electric board — is not unwarranted given the crisis faced by top unicorns Byju’s and PharmEasy.

PharmEasy raised $350 million in Series E (equity) round in April 2021. This was followed by a rather unusual and audacious step to raise Rs 2,280 crore [$285 million] debt from Kotak Mahindra Bank to fund Thyrocare’s acquisition in May 2021. Now a couple of years later, the founders’ reluctance to dilute equity has backfired as the company is looking to pay off its debt with a rights issue and at a much lower valuation. All to prevent the firm from slipping away completely from their hands, even as their own stake becomes almost inconsequential in the larger scheme of things.

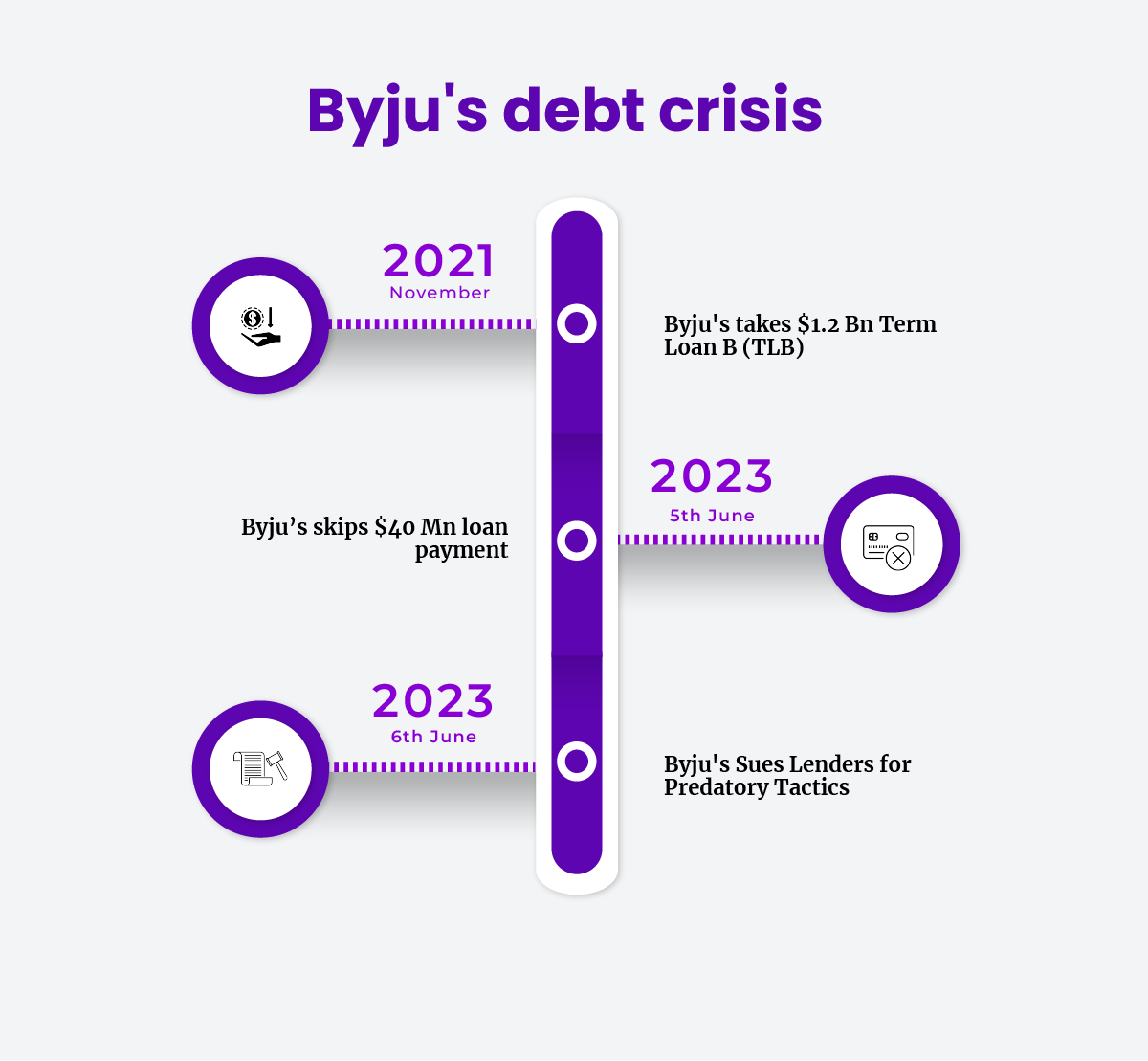

In a similar vein, Byju’s took a $1.2 billion term loan B for a tenure of five years with a yield to maturity (YTM) of 6.78% in November 2021. Byju’s is currently locked in a legal tussle over alleged debt default.

It is natural for the startup ecosystem, especially after these two high-profile incidents, to steer away from collateral-based or term loans for capital. However, sentiment was not the same a couple of years ago. Also, term loans were available to startups at a relatively cheaper coupon rate during the 2021-22 period.

“At that time, going the debt route instead of equity seemed [like] a wise move for many as equity capital was available in abundance,” said the unicorn founder. One might add, not just in abundance, but with a generous jump in valuations with each round. Far higher than the rate of interest on debt, or so the founders thought.

“A lot of our portfolio companies [in growth stage] approached us for advice on whether they should raise term loans or not. The answer was not at all because their bottomline was in the red,” he added.

Conceptually, term loans are not a bad thing. Such loans help startups fund acquisitions and plug working capital requirements. But there is a catch: doing so without a clear sight of a cash inflow in the coming months could deal a severe blow.

Ashish Fafadia, CFO of early-stage VC firm Blume Ventures, says the ideal usage of debt capital is for the working capital, which is money deployed towards ensuring operations run uninterrupted. “I do feel that the startups do best when they use debt meaningfully… Anything beyond that definitely creates a bit of a challenge,” he said.

Abhay Pandey, partner at growth-stage venture capital firm A91 Partners, suggests a cautious approach.

“Borrowing money against your equity as collateral is a very risky strategy. I think most founders will not do it and most boards will not recommend it,” he told Entrackr.

Pandey further said that startups thought that their equity value was inflated but they didn’t realize it while lenders took collateral and thought that they were very secure.

“Both [startups and lenders] were wrong. Companies were also wrong to borrow large loans for acquisitions because they thought we can buy something and then I get valued more because I’m buying something with cheaper valuations,” he added.

When asked whether companies which raised collateral loans by pledging their shares will get a valuation correction?

Pandey said, “It is case by case, but if you have raised a lot of debt based on some last term valuation and you have to repay that debt by raising equity or some cash flows. It could be very hard.”

Quite simply, the fixed nature of debt, and it’s coming at a very low cost (till recently), seduces many founders into complacency, thinking that if push comes to shove, they can always raise fresh equity to repay. However, as most have discovered, if the market sours so far that easy debt is not available, then equity valuations can never survive such a market too.

Debt, if at all, should perhaps be taken from the equity holders only, in the hope that they will get more flexibility and forbearance in case of a temporary glitch. Otherwise, it is best avoided unless you have the cash flows for it. A short term bridge round of debt while expected equity inflows came through the paperwork was the preferred route till a few years back. It would be safe to say that in this case, the ‘traditional’ way makes more sense.