National Payments Corporation of India (NPCI) has been leading the proliferation of digital payments in the country from the front and manages a bunch of payment systems including IMPS, UPI, BHIM, NACH, RuPay, AePs, FASTag and BBPS among others.

While NPCI dominates media every now and then for volume and value processed through the above payment systems, innovation and creating one of the most robust and simple payments stacks: UPI, its financial performance has never been analyzed at length.

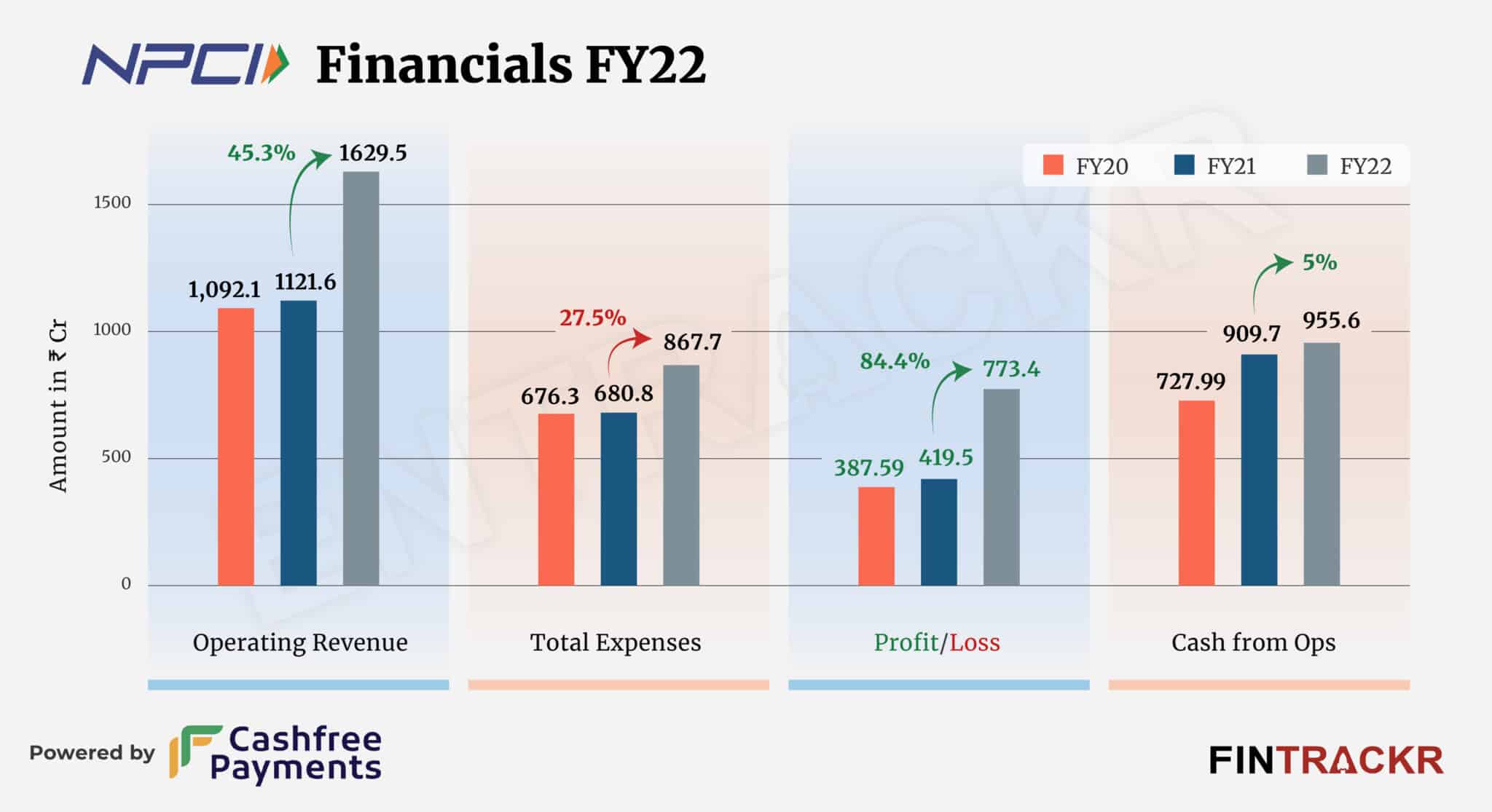

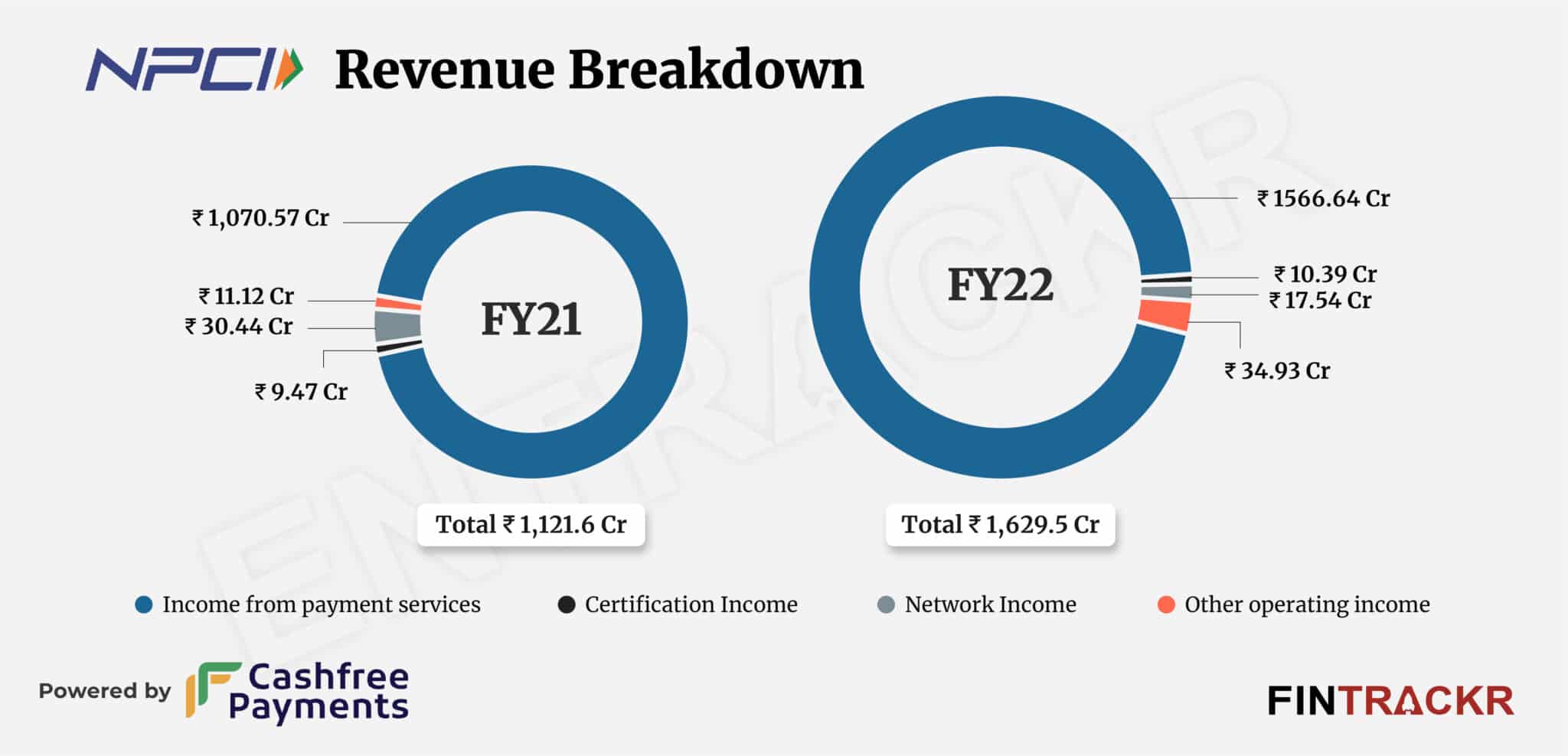

Fintrackr has sifted through its annual financial statement for FY22 and found out that its operating revenue grew 45.3% to Rs 1,629.5 crore during FY22 from Rs 1,121.6 crore in FY21.

Income from payment services constituted 96.1% of NPCI’s operating revenue which surged 46.3% to Rs 1,566.64 crore in FY22.

Its certification income grew by 9.7% to Rs 10.39 crore while network income dipped 42.4% to Rs 17.54 crore during FY22. The company made another Rs 34.93 crore from ops which includes compliance and membership fees, income from international alliances, hologram charges, and card fees.

The company also has other income (non-operating) of Rs 230.6 cr during FY22 mainly from interest on current investment.

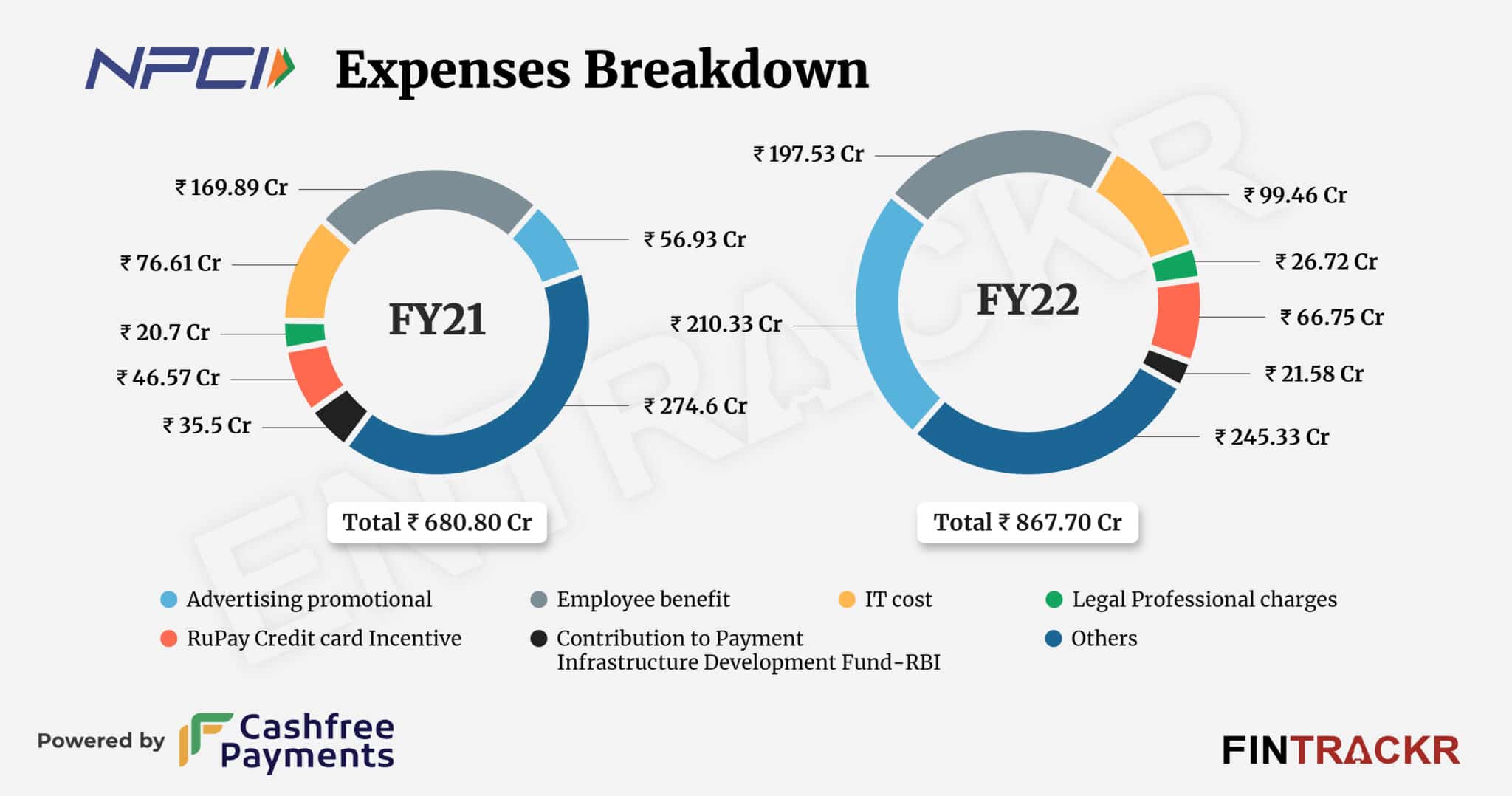

With various programs for consumer awareness to encourage retail payments in India through its products, its advertising and promotion costs formed 24.2% of the firm’s overall expenditure. This cost grew over three-fold to Rs 210.33 crore in FY22 from Rs 56.93 crore in the previous fiscal year.

Its employee benefit cost increased 16.3% to Rs 197.53 crore in FY22 from Rs 169.89 crore in FY21 whereas spending on information technology and incentive on RuPay cards surged by 29.8% and 43.3% to Rs 99.46 crore and Rs 66.75 crore respectively.

NPCI incurred Rs 26.72 crore and Rs 21.58 crore against legal-professional fees and contributions to Payment Infrastructure Development Fund-RBI which pushed its overall cost by 27.5% to Rs 867.7 crore in FY22.

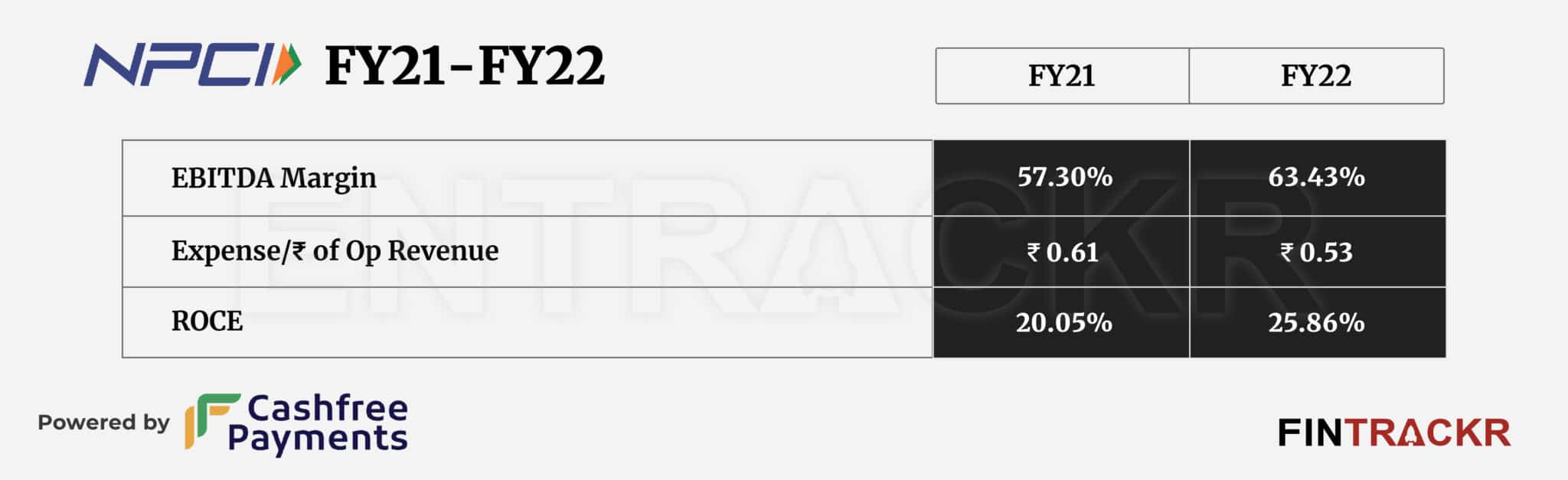

In the end, the company’s profit spiked 84.4% to Rs 773.4 crore in FY22 from Rs 419.5 crore in FY21. Its ROCE and EBITDA margin remained positive with 25.86% and 63.43%. On a unit level, NPCI spent Re 0.53 to earn a single unit of operating revenue in FY22.

Backed by a cohort of 66 shareholders including public sector banks, private banks and other players in the financial services sector, NPCI certainly delivers as an investment to its stakeholders. However, its performance as a partner that oversees some of the biggest innovations in the sector is up for debate, considering how ‘stingy’ it has been when it comes to allowing profits to be made on these innovations. All the more reason to track and ensure that the ‘ecosystem’ behind NPCI and the tremendous influence it has does not stifle potential innovators or innovations elsewhere.

The thing about the financial sector is that even as you have UPI at one end with its superb delivery at zero cost to end users, you also have, say, forex transactions where the charges are usurious, to say the least. And this is despite RBI supervision of the banks that charge these rates. NPCI, in many ways, has upended the easy profits and growth VISA and Mastercard were enjoying in credit cards. It is important that NPCI itself does not turn into precisely the entities it disrupted with the UPI stack.