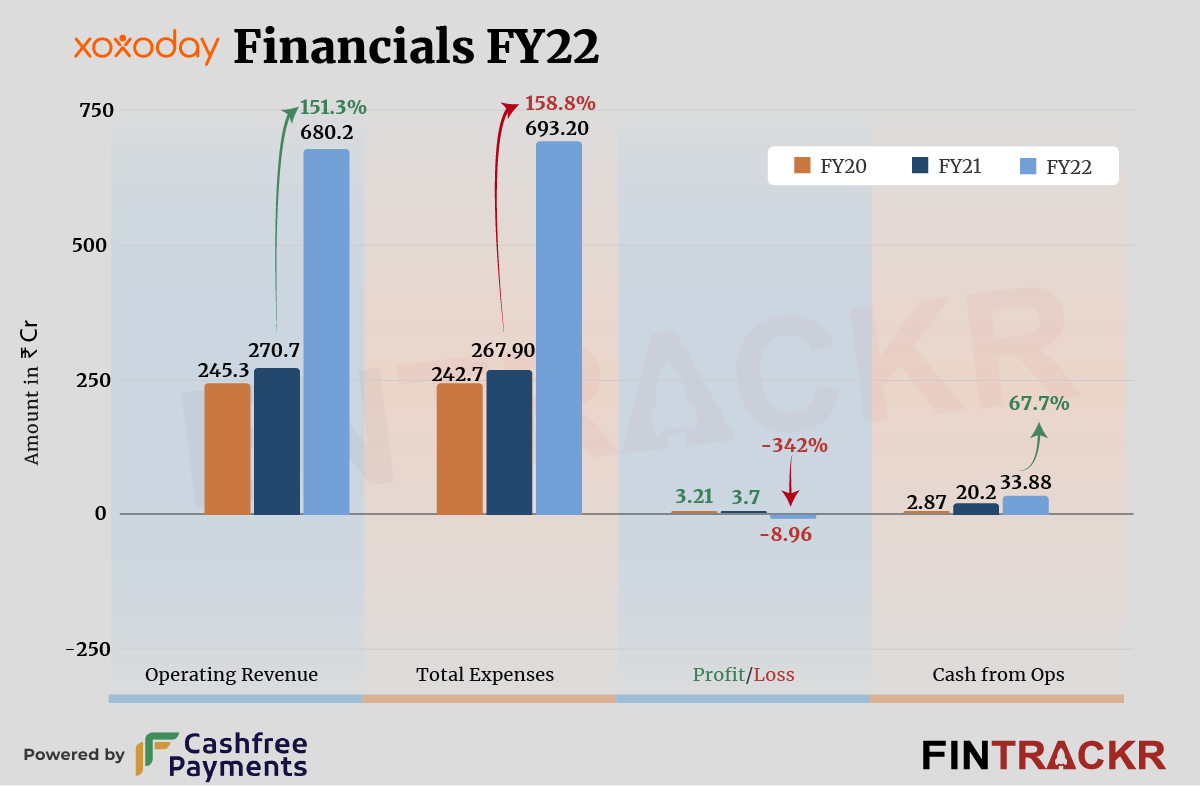

Following a flat 10% growth in FY21, fintech firm Xoxoday ended FY22 with a more than two-fold gain and revenue nearing the Rs 700 crore mark. The company, however, also slipped into losses in FY22 owing to expenditure on coupons and rewards eclipsing the revenue growth.

Xoxoday offers technology infrastructure which lets businesses automate rewards, incentives, and payouts across the value chain. Its product portfolio consists of Plum, Emplus, and Compass for rewards, employee engagement, and incentive computation.

Collections from the sale of products were the sole source of revenue for Xoxoday which surged 2.5X to Rs 680.2 crore in FY22 from Rs 270.7 crore in FY21. It also generated an interest income (non-operating) of Rs 1.32 crore during FY22.

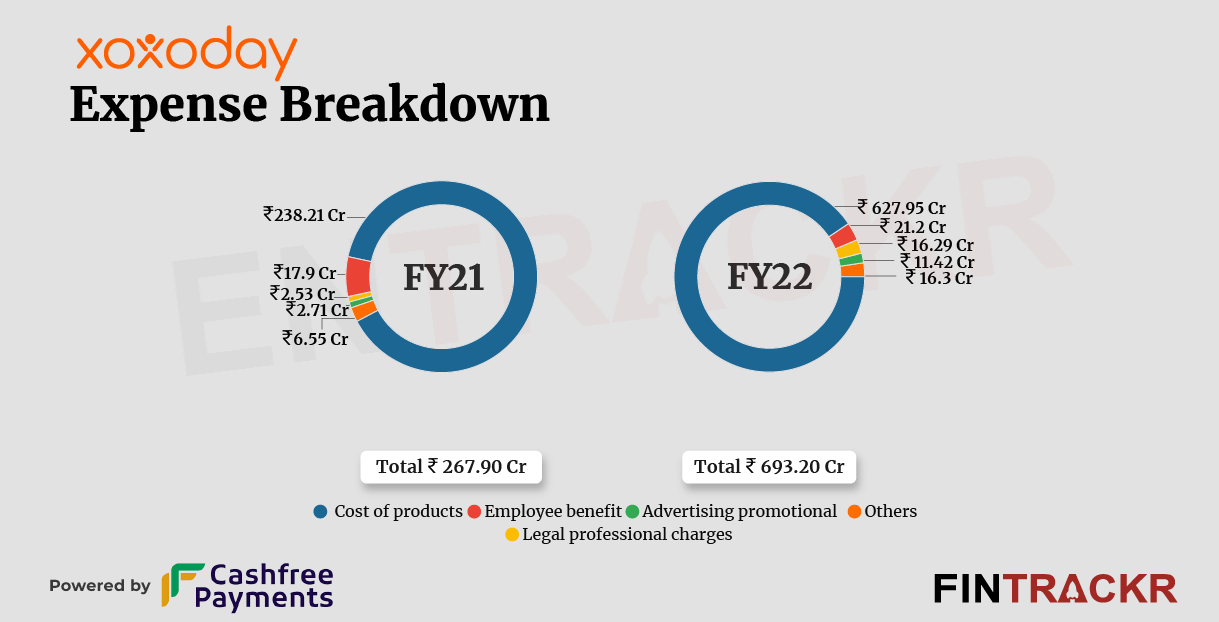

On the cost side, the purchase of coupons and rewards from the brands accounted for 90.6% of the total expenditure. This expense grew 2.6X to Rs 627.95 crore in FY22 from Rs 238.21 crore in FY21.

Unlike most growth and late-stage startups, its employee benefit cost barely increased by 18.7% to Rs 21.2 crore in FY22.

Legal-professional and advertisement costs jumped 6.4X and 4.2X to Rs 16.29 crore and Rs 11.42 crore, respectively, in FY22.

At the end, Xoxoday’s overall cost shot up 2.58X to Rs 693.2 crore in FY22. While the company was profitable for consecutive fiscal years (FY20 and FY21), it turned into the red in FY22 with a loss of Rs 8.96 crore.

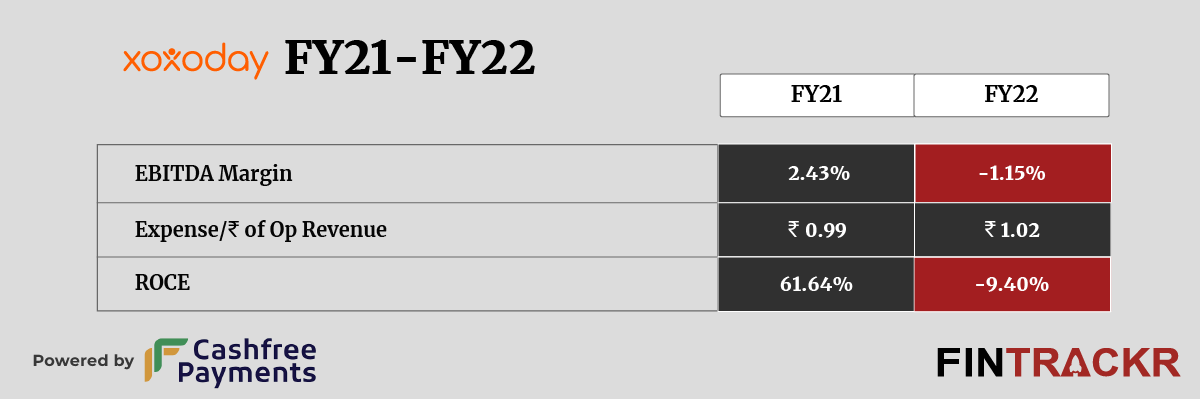

Its ROCE and EBITDA margin stood at -9.40% and -1.15%, respectively, in FY22. On a unit level, the company spent Rs 1.02 to earn a single unit of operating revenue.

The slippage into losses is no surprise, considering the razor-thin margins the business operates on. The share of purchase of coupons and rewards also makes it clear the firm is more about running the programs itself than just an infrastructure provider.

Xoxoday has a strong portfolio of clients and well-controlled costs, but it clearly has to worry about a weak moat when it comes to protecting against the competition. This is a business that is most susceptible to acquisitions by larger players, and it should be interesting to see how Xoxoday confronts its future.