E-sports and skill gaming platform Mobile Premier League (MPL) turned unicorn in September last year after raising its Series E round led by Legatum Capital, managing to scale its valuation 2.4X to $2.3 billion within 7 months.

The Bengaluru-based company claims to have over 9 crore users on its platform and offers more than 60 online games such as Fantasy Cricket, Rummy, Speed Chess with real cash prizes in paid tournaments and 1V1 games. With the steep rise in its valuation, MPL’s scale also blew over 8X in FY21.

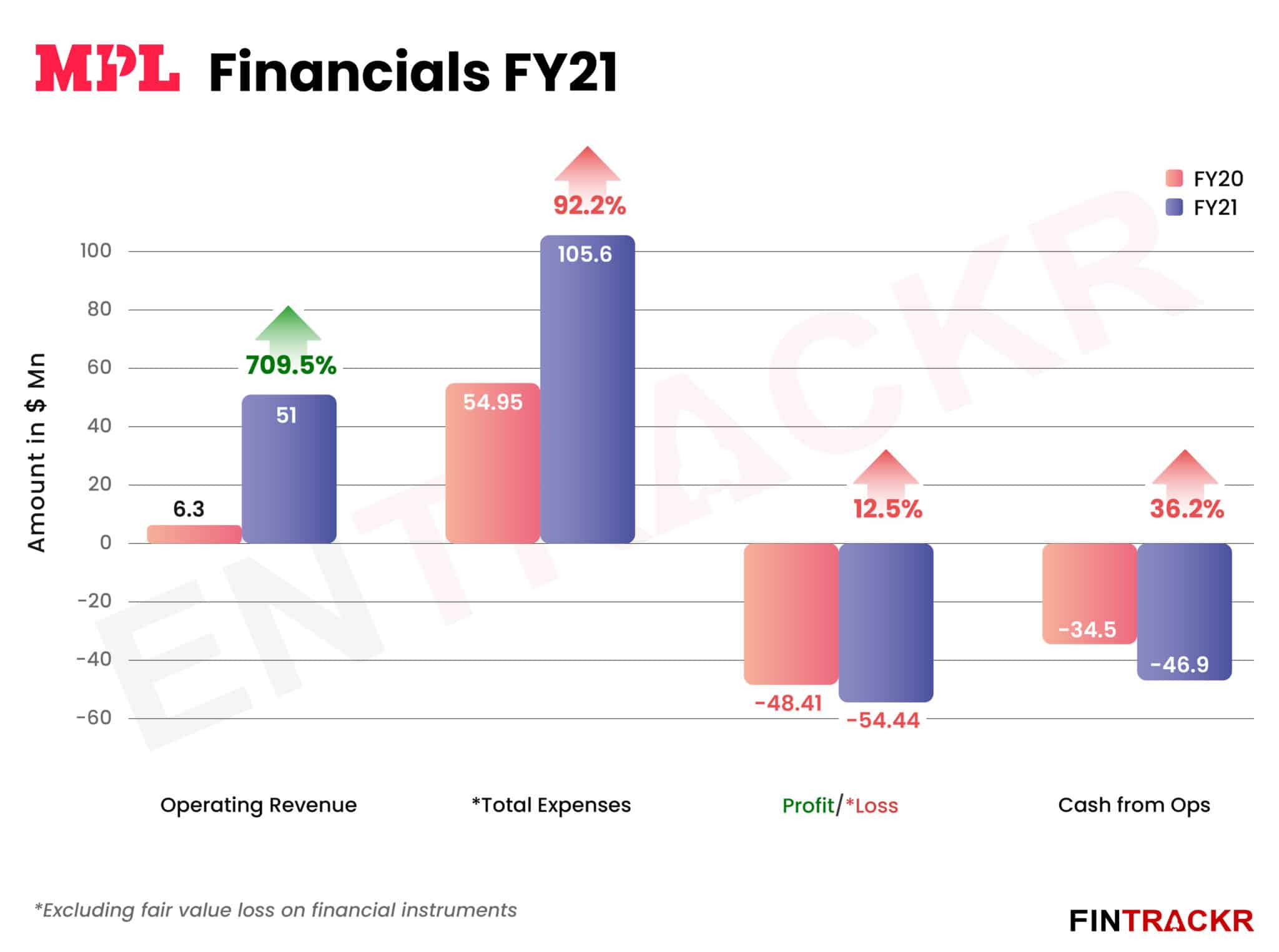

During the fiscal marred with Covid-19, the gaming company has managed to grow its revenue from operations by 709.5% to $51 million from $6.3 million in FY20, as per its annual statements filed by its holding company M League Pte in Singapore.

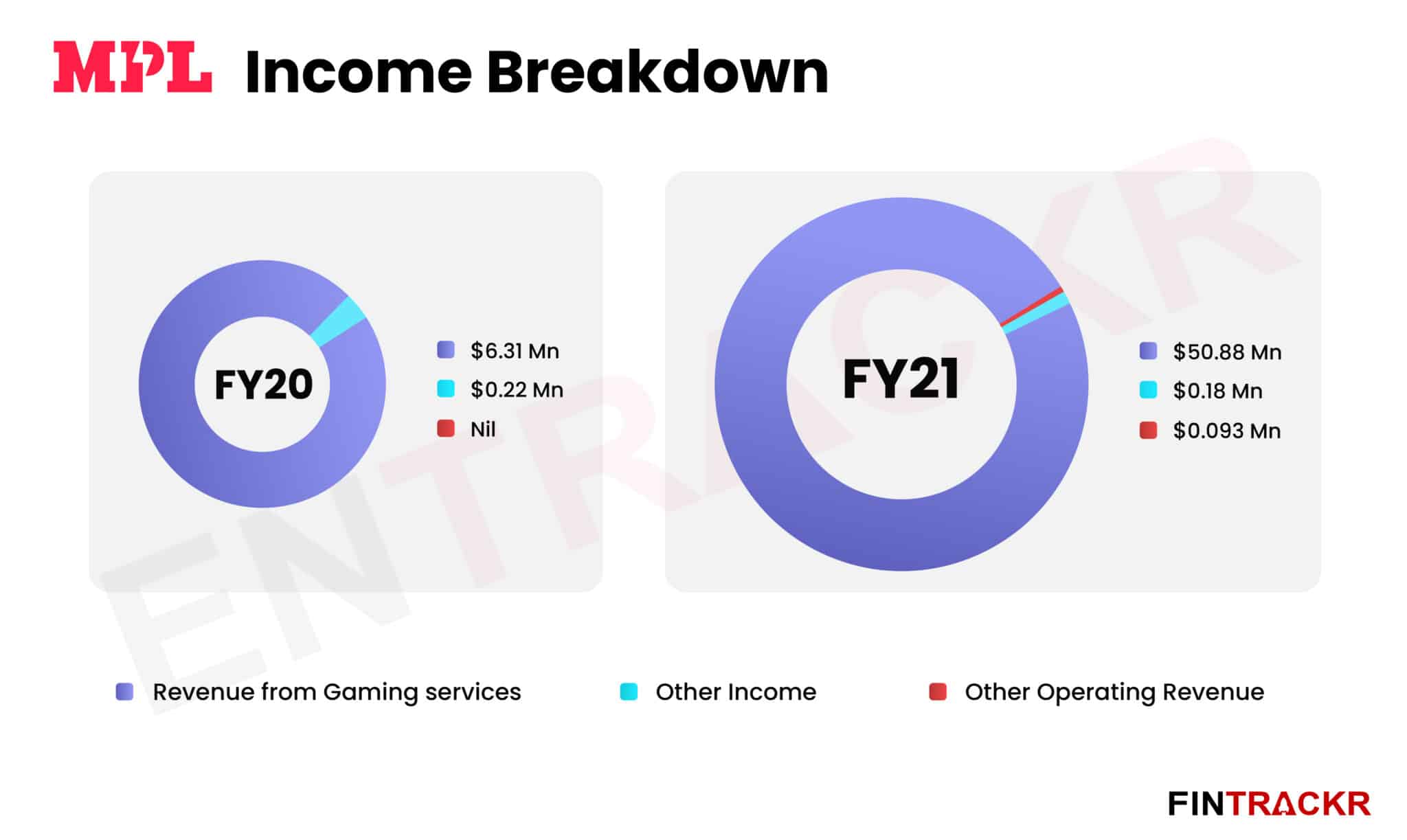

The company has generated 99.5% of its income from gaming services. This includes the entry fee for the games on its platform which it books as revenue. Such revenue grew by 706.3% YoY to $55.88 million in FY21. The company also has a merchandise vertical MPL Sports which is the official kit partner of the Indian Cricket team. Fiscal 2020-2021 was the first year of operation of this vertical and the company sold merchandise worth $93.7 K during this period.

The company also collected non operating income of $182K from its financial assets during FY21.

A major reason for the company’s growth was its aggressive customer acquisition strategy utilizing social media channels and television ad placement during major cricket tournaments.

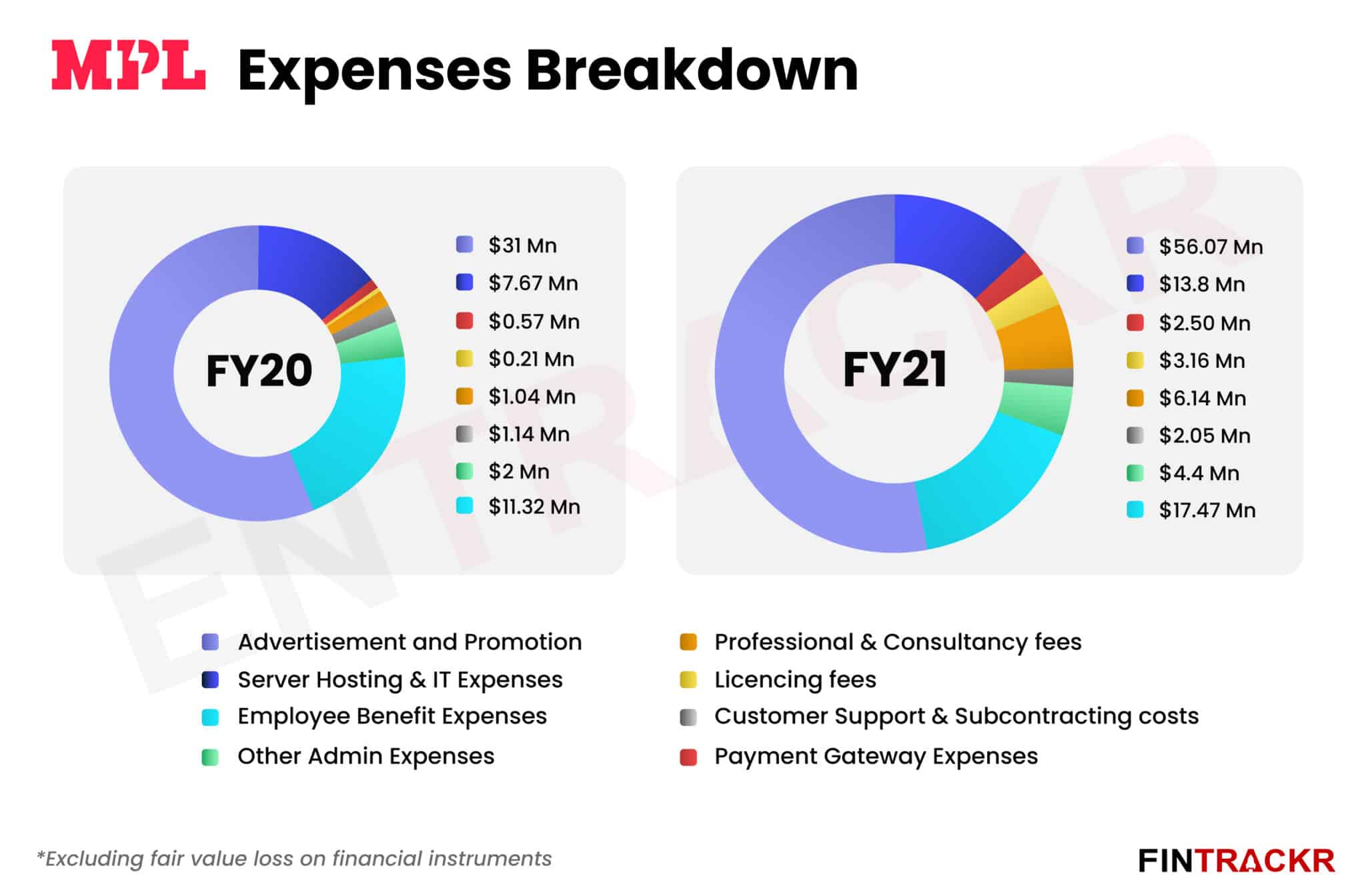

Advertising and promotions were the largest cost centers for the gaming company, accounting for 53.1% of its annual costs. These costs surged by nearly 81% to $56.07 million in FY21 from $31 million in FY20. These also include sponsorship expenses of $3.7 million.

The company also provides incentives and discounts to users to promote engagement which amounted to $20.92 Million in FY21, growing by 102% from rewards worth $10.35 million given away during FY20. These payments are deducted from gross collections before revenue is booked.

The growth in scale is also evident from its payment gateway costs which grew by 338.6% to $2.5 million in FY21 from $577K spent on the same during FY20 as the volume of transactions grew multi-fold on its platform. During the same period, server hosting and IT expenses also surged by 80% YoY to $13.8 million in FY21 and made up 13.1% of MPL’s annual costs.

The company also increased its employee base with employee benefit payments accounting for 16.5% of its annual expenditure. Such payments grew by 54.3% from $11.32 million in FY20 to $17.47 million during FY21 which also included share-based payments of $4.1 million.

Moving further down the expenses sheet, we observe that MPL’s payments towards licensing fees ballooned by 1404.8% YoY to $3.16 million while professional consultancy costs surged by 490.4% YoY to $6.14 million during the fiscal ended in March 2021.

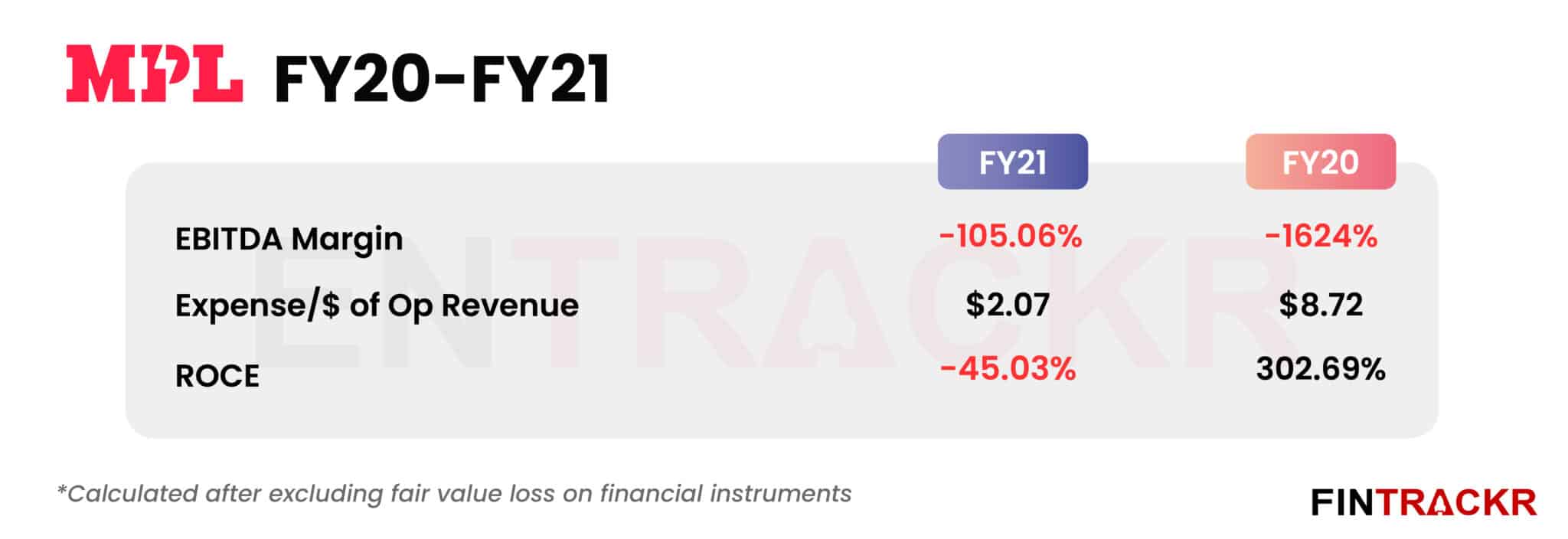

MPL also spent $27.8K on procurement of merchandise which pushed its annual expenditure to $105.6 Million in FY21, growing by 92.2% as compared to $54.95 Million spent in total during FY20. The gaming company spent $2.07 to earn a single dollar of operating revenue, improving by 76.3% as compared to $8.72 it spent to earn the same in FY20.

The exponential growth in collections was also visible in the EBITDA margin which improved from -1624% in FY20 to -105 % during FY21. Even with seven folds growth in scale of operations and nearly doubling its cashburn, MPL’s annual losses have grown by only 12.5% to $54.44 Million during FY21 from $48.41 million lost in FY20.

At almost a seventh the size of market leader Dream 11 in terms of revenues, MPL is playing in a market that is hugely competitive, with innovation at a premium. The market leader being profitable also makes it essential for the challenger firm to carve out its space to play and position itself quickly for a long stint, much like the players in many of its games.