Payment aggregator platform BharatPe became the 19th unicorn startup in India a fortnight ago after raising $370 million in its Series E round led by Tiger Global. The mammoth funding round was raised at a valuation of $2.85 billion, making BharatPe the fifth most valued fintech company in India after Paytm, PhonePe, Razorpay and Pine Labs.

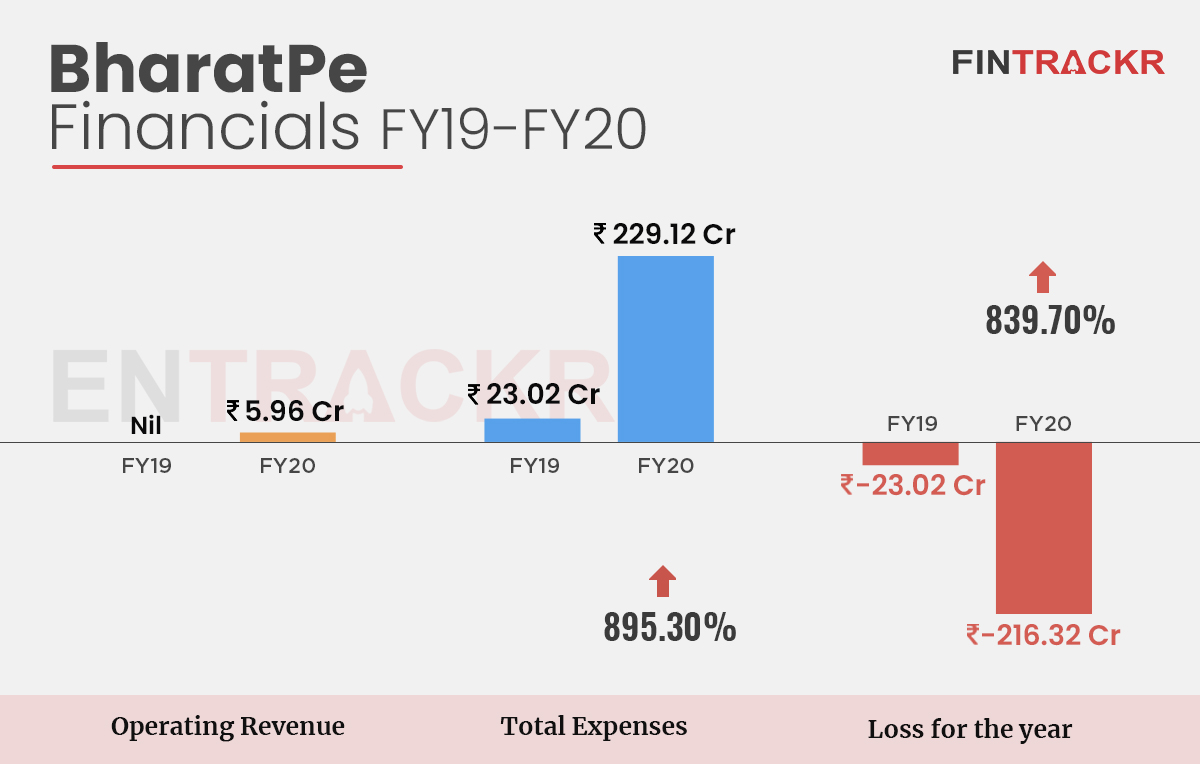

Right before the announcement of this fundraise, the company had claimed that its annual revenues grew 7X to Rs 700 crore in FY21 from around Rs 110 crore earned during FY20. While the company is yet to file audited numbers for the last fiscal, the company has submitted its annual statement with RoC for FY20.

Fintrackr took a deep dive to understand BharatPe’s financial health.

The growth-at-all-costs mantra

Resilient Innovations Pvt Ltd, the holding entity of BharatPe and its lending operations earned revenue of Rs 5.96 crore during FY20, as opposed to FY19 when they did not earn any operating revenue. This income was primarily generated by providing small ticket unsecured loans to merchants and collecting commissions on transactions.

The loans were sourced from its subsidiary Resilient Capital Private Limited which was incorporated in May 2019 and earned profits of Rs 8.05 lakh during its first year of operations. Notably, BharatPe had claimed that it had disbursed loans amounting to Rs 150 crore to its member merchants during FY20.The company also earned Rs 6.94 crore from its financial assets during the same period.

While revenues were limited in FY20 as it was only the second year of operations for the company, BharatPe burned through a lot of cash to establish itself in the hyper-competitive Indian payments sector. The company saw its annual expenditure jump by 895.3% to Rs 229.12 crore during FY20 from Rs 23.02 crore in FY19.

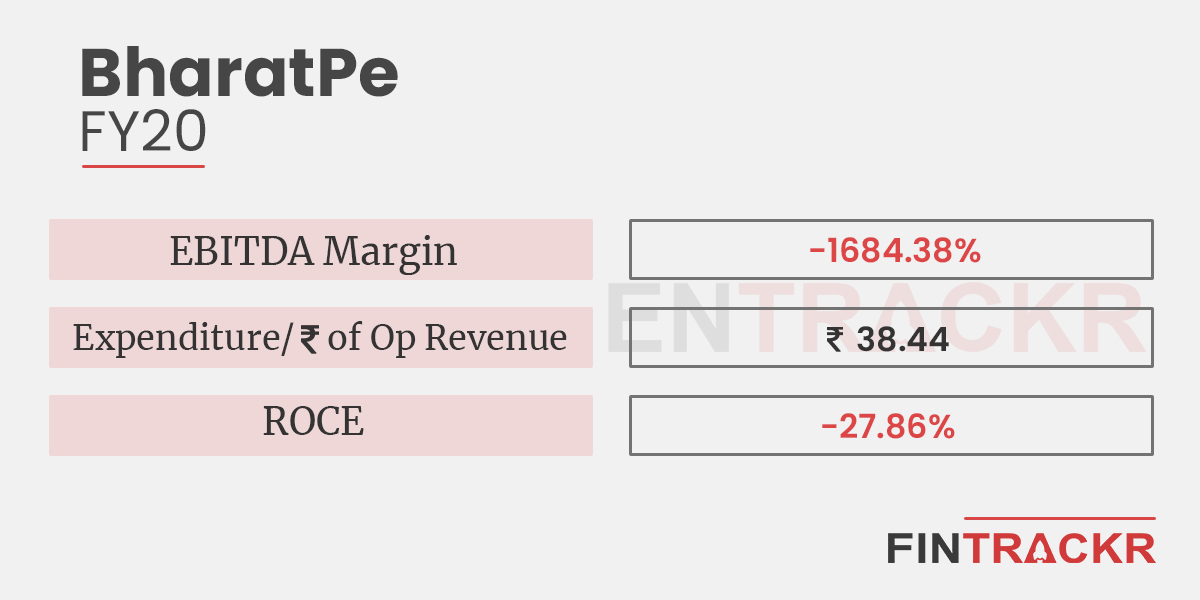

On a unit level, BharatPe spent Rs 38.44 to earn a single rupee of revenue during the fiscal year ending in March 2020.

Rs 142 Cr as miscellaneous expense

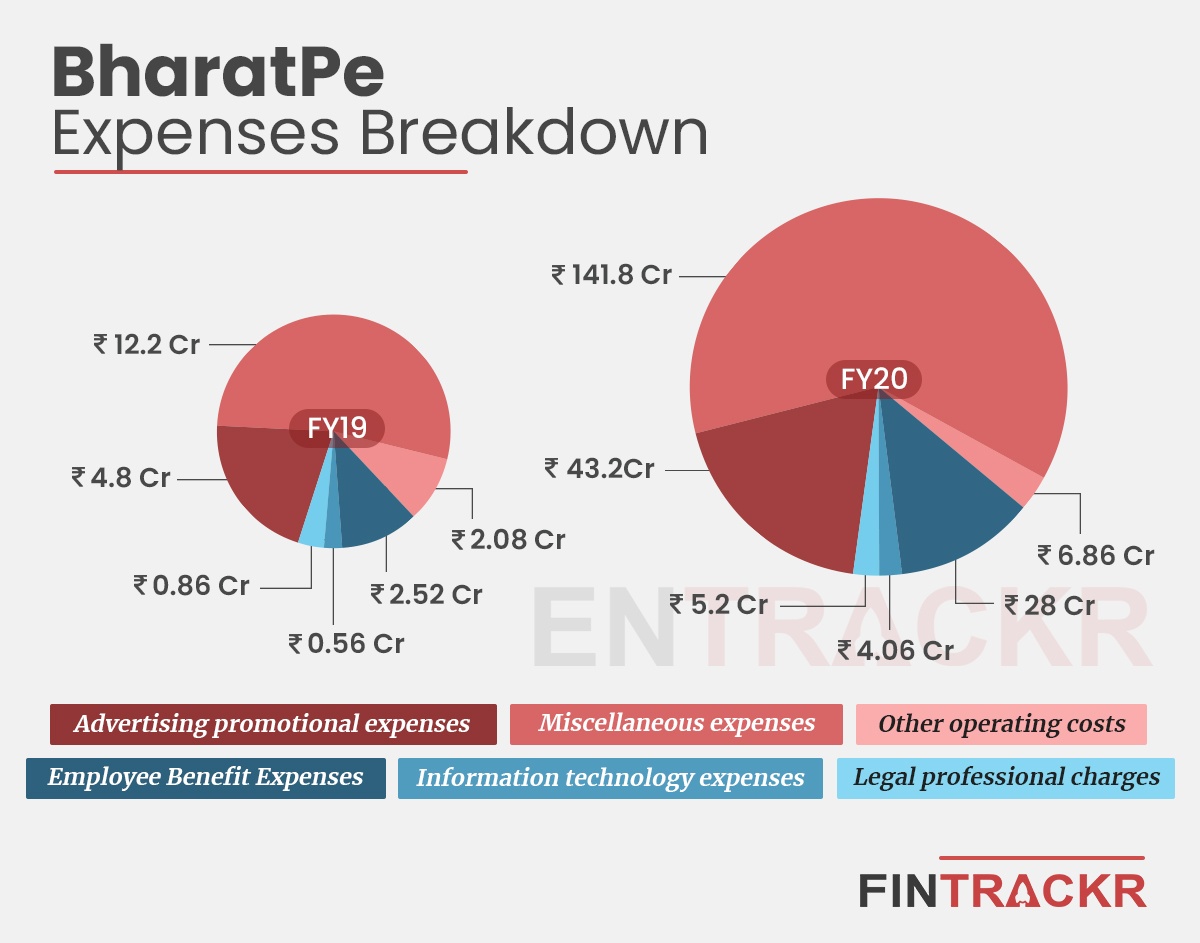

Moving over to the expenses sheet the single largest line item was booked under “Miscellaneous Expenditure” which accounted for nearly 62% of the annual cashburn. These expenses had blown up 11.6 times to Rs 141.8 crore during FY20 from Rs 12.2 crore in FY19.

When reached out by Entrackr, BharatPe has refused to comment on the nature of the unexplained miscellaneous expenses on its income statement and the story. However, it appears that these comprise the payment processing charges (including MDR) incurred by the company among other growth focussed capex.

BharatPe claims to have boarded around 24 lakh merchant members on its platform by the end of FY20. And, these merchants’ acquisitions came at a cost: it spent heavily on customer acquisition and brand development as advertising and promotion cost stood out as the second-largest burn for the Delhi-based company.

Such expenses shot up 9X to Rs 43.2 crore during FY20 from Rs 4.8 crore spent on the same during FY19.

The Ashneer Grover-led company was recently in news for its unconventional talent acquisition strategy earlier this year, offering high-end BMW bikes, gadgets and an overseas trip to new joinees in the tech and product teams. These expenses will surely bloat up this fiscal’s employee benefit expenses. Meanwhile, for FY20, its employee benefit costs made up 12.2% of annual costs, growing 11.1X to Rs 28 crore during FY20.

Further, BharatPe’s IT costs jumped 7.3X to Rs 4.06 crore whereas legal and professional costs shot up 6X to Rs 5.2 crore during FY20.

During FY20, BharatPe posted an annual loss of Rs 216.32 crore, ballooning 9.4X from the Rs 23.02 crore in FY19. With an abysmal EBITDA margin of -1684.4% during FY20, the present cash burn appears tough to sustain for the growth stage company.

Will BharatPe achieve Rs 700 Cr revenue in FY21?

The FY20’s numbers for BharatPe outline that the company was chasing growth (merchants) at all costs. This growth was intended and worked well for the company: it brought much-needed momentum leading to three fundraising events in which the company cumulatively mopped up close to $615 million.

Even as BharatPe’s financial performance looks underwhelming in FY20, things may be different moving forward as the company added several layers of monetisation in FY21 such as point of sale (PoS) business and lending. In the ongoing fiscal, the company began peer-to-peer (P2P) lending and is also likely to start PMCBank operations in partnership with Centrum. These channels are bound to fill up the company’s revenue coffers in FY21 and in the ongoing fiscal (FY22).