Mobile development startup PlaySimple’s acquisition by the Swedish gaming firm Modern Times Group (MTG) for a whopping $360 million last week was the biggest news for the Indian startup ecosystem in 2021 for several reasons. For starters, unlike most acquisition deals, this one is majorly a cash exit where every stakeholder made a killing.

Moreover, the company raised a total of $4.5 million since its inception in 2014 and turned profitable in FY20 with Rs 38 crore in the green. Founded by former Zynga employees Suraj Nalin, Siddhanth Jain, and Preeti Reddy and former Walmart Labs employee Siddharth Jain, PlaySimple operates multiple word games including ‘Daily Themed Crossword’ and ‘Word Wars.’

To understand the structure, its financials and the kind of return its stakeholders have made from this under-the-radar startup, Fintrackr sifted through its regulatory filings sourced from both Singapore and India.

Small investment, bumper returns

The year 2014 was when PlaySimple launched and also raised its first funding round. In December 2014, the company raised Rs 3.14 crore from Chiratae Ventures, Pandara Trust and Yezdi Lashkari who was then working with Microsoft’s Venture accelerator and went onto launch his own venture FlexMoney in 2015, filings show.

Two years later in November 2016, PlaySimple raised Rs 27 crore in Series A round from SAIF Partners (now Elevation Capital), Chiratae Ventures and Pandara Trust at a valuation of Rs 115 crore.

Their investment journey was short and ended there.

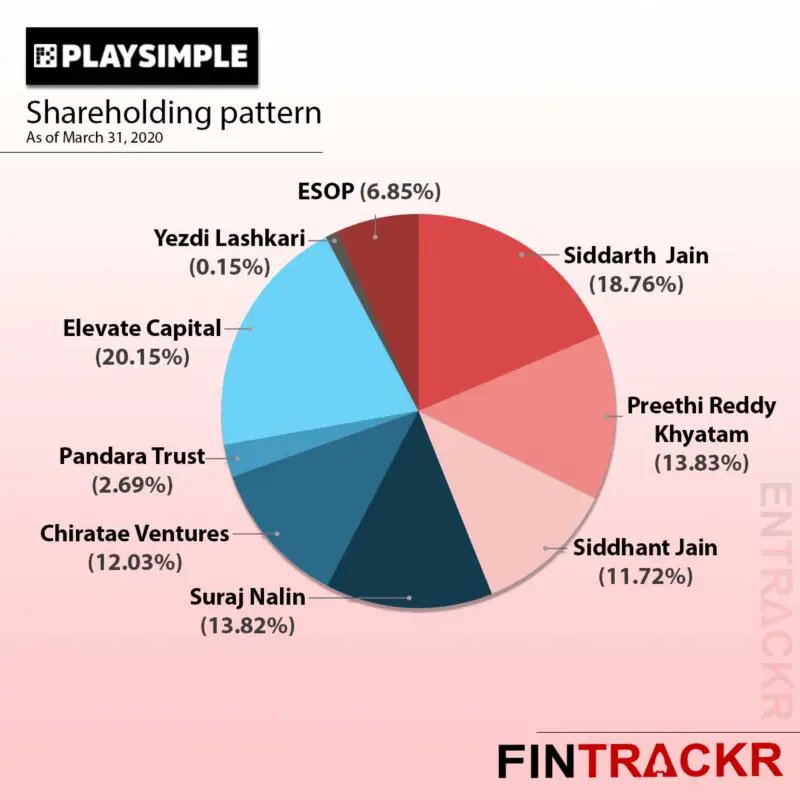

Following these investments, the co-founders together owned 58.13% of the company, after accounting for the notional ESOP Pool created by the company which has 23,387 options each convertible into an equity share of the company.

Fintrackr’s calculation places Elevation Capital as the biggest stakeholder among the company’s investors, controlling nearly 20% stake in the gaming company, followed by Chiratae which commands 12.03%. Early investor Pandara Trust holds around 2.69% stake in the business.

With a partial cash liquidity event, around 77% of the acquisition consideration of $360 million will be divided as per each shareholder’s stake in PlaySimple. The promoters are likely to receive around $155-$161 million: while brothers Siddarth and Siddhant Jain are likely to cash in $52 million and $32 million, respectively, Suraj Nalin and Preethi Reddy are likely to receive $38 million each.

Caveat: these are mean estimates based on their shareholding pattern and may vary slightly during the actual cash disbursement.

As for Elevation and Chiratae — they are looking to pocket around $58.5 million and $33.4 million, respectively. On the other hand, Pandara Trust and Lashkari will receive around $7.4 million and $415K, respectively from their stake sale.

PlaySimple’s playbook: Growing from Rs 27 Cr to Rs 330 Cr in 3 years

PlaySimple witnessed explosive growth in the last three years and turned profitable in FY2020. Let’s take a look at how they made this happen.

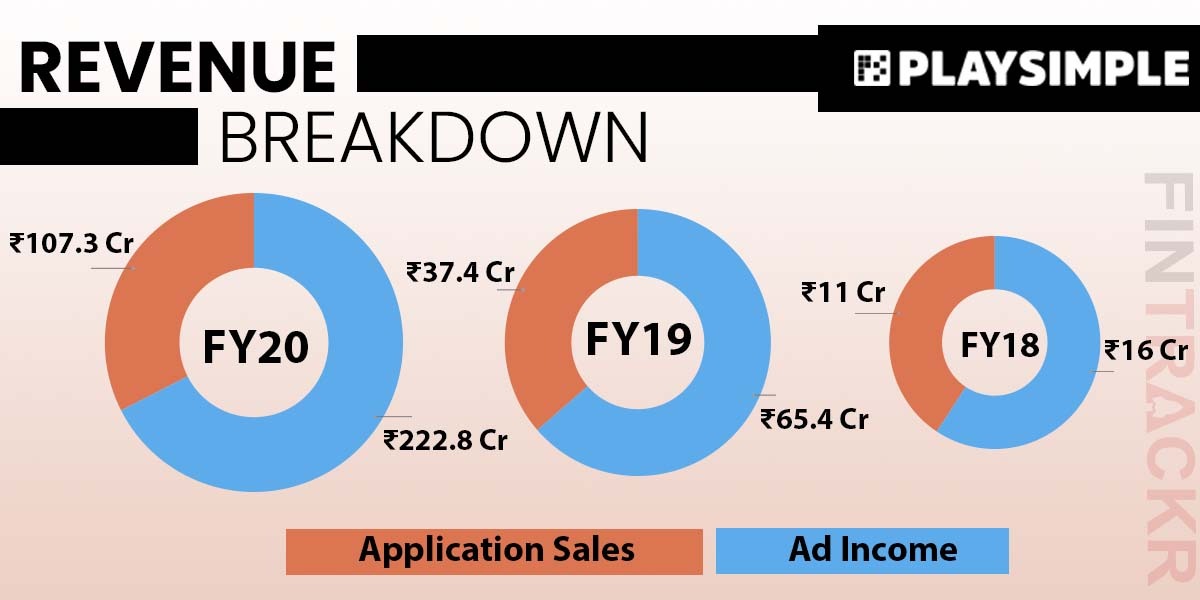

The gaming company generates its revenues primarily through the sale of advertising space and application income generated through the sale of digital content through mobile platforms.

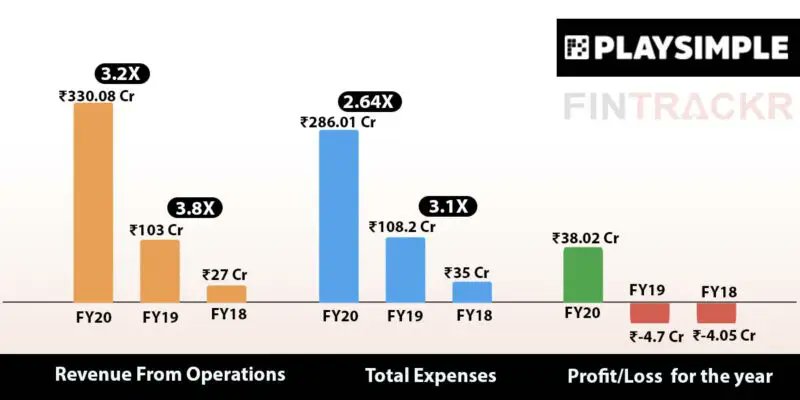

PlaySimple made only Rs 27 crore in operating revenue in FY18 which soared by 280% to Rs 103 crore in FY19. And in the fiscal year ending in March 2020, the company saw its revenue jump 3.2X year-on-year (YoY) to a little over Rs 330 crore, essentially growing 12.2X within a span of 36 months.

With the acquisition amount pegged at $360 million, the company has been acquired at a revenue multiple of 8X.

During the last reported fiscal year, i.e. FY20, PlaySimple had earned 67.5% of its operating revenue from advertising and the rest 32.5% from application sales. Let’s glance over at the revenue breakdown during the last three fiscal years:

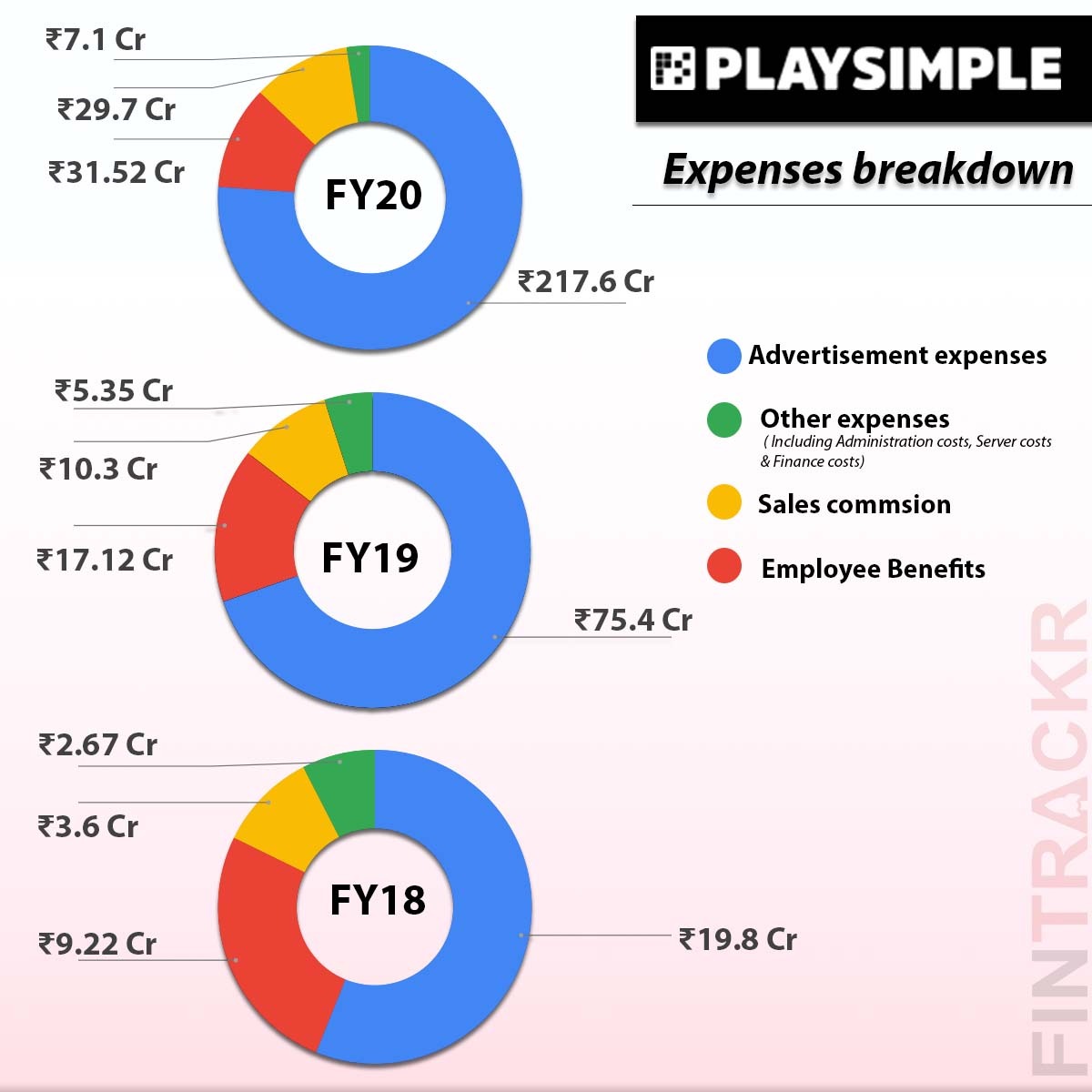

Moving over to the expenses, we see that advertisement expense is the largest cost center for the gaming company and grew in line with the revenues. These costs accounted for 76% of the total expenses incurred, growing around 11X from Rs 19.8 crore in FY19 to Rs 217.6 crore during FY20.

Employee benefit expenses were the second largest expense for the mobile gaming company, growing by 242.4% from Rs 9.2 crore in FY18 to Rs 31.5 crore in FY20. Sales commission payments came out at a close third, growing by 725% from Rs 3.6 crore paid in FY18 to Rs 29.7 crore during FY20.

During the fiscal year ending in March 2020, PlaySimple spent Rs 286.01 crore in total, 717% more than the aggregate costs of Rs 35 crore spent during FY18. During FY20, PlaySimple spent Rs 0.87 to earn a single rupee of operating revenue.

Essentially, FY20 is the year when the company saw a financial turnaround: from incurring a loss of Rs 4.01 crore in FY18 to posting a post-tax profit of Rs 38.02 crore in FY20 at an EBITDA margin of 14.42%.

PlaySimple has been quietly building its company over the years with little exposure in the media. This acquisition news definitely gives flashbacks to 2020 when edtech startup WhiteHat Jr was bought by Byju’s in the largest cash exit at the time of $300 million. There are similarities: the Karan Bajaj-led company also didn’t raise a lot of capital and focused on generating revenue.

PlaySimple’s playbook was simple: prioritise revenue and grow it without raising too much external capital or chasing vanity metrics such as valuation. It’s certainly an inspiration for many to create large companies with little money and complete control.