There is no denying that in the past couple years, turning a billion-dollar worth startup and coveting the so-called prestigious Unicorn status has resulted in a cut throat rat race where entrepreneurs, investors, as well as the media and the audience, all are equally obsessed with the tag.

“In the latest round of funding with $X million more in the pocket, Y is now valued at more than $1 billion and is now a Unicorn.”

“Valued at over $1 billion, Z is now the fastest unicorn in the startup ecosystem.”

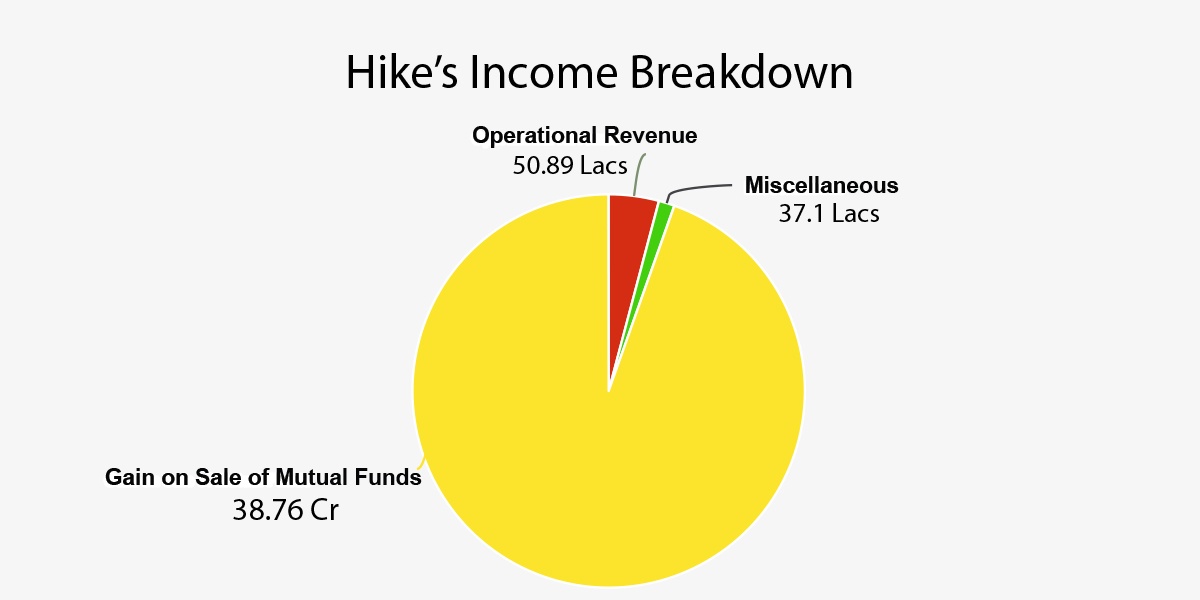

Well, as of now, in the B2C segment, the fastest Unicorn is Ola Electric, but until a month ago that title sat on Kavin Bharti Mittal’s mantle, vis-a-vis Hike. A company, that in FY18 had lost Rs 400 crores, and earned Rs 39.64 crore out of which 97.8% was just profit on the sale of mutual funds, and only Rs 50.8 lakhs organic revenue from financial services.

A 2012 founded company, five years into operation in 2017, with no dearth of funds (the CEOs father owns the third largest telecom company by users) and a Unicorn tag, loses Rs 400 crore to earn Rs 50.8 lakhs from its core services makes us ask one question – How does one ever justify that mighty valuation?

This article is about questioning the relevance of these market cap valuations that the investors and the company arrive at during the due diligence process before any funding round, or in the normal operations of a firm where valuation is calculated annually, half-yearly, or sometimes quarterly.

Most firms use the Discounted Cash Flow method to estimate these valuations. For a brief idea, this method entails making periodic projections of the financial statements for a certain time period (subjective) and then discounting the value of the company on the basis of the last future projection, post certain adjustments.

Basically, the firm projects its own financial health on a future date and calculates the present value of that health.

Hike was founded in 2012, it became a unicorn in 2016 – in merely 4 years (even though that sounds like a long period considering Ola Electric’s half a year-long journey to the title). If in 2016 the company calculated the $1 billion valuation on the basis of this method, the due diligence could not have projected a Rs 400 crore loss and Rs 50.8 lakhs in organic revenue for FY18. But that is exactly what happened.

ShopClues and Disinvestment

Now if that doesn’t tell you how the vanity of being a Unicorn is useless until and unless a startup actually delivers on what it projects, I’m sure the case of ShopClues will. The company just shut down operations by handing pink slips to over 200 people after failed acquisition talks with major e-commerce companies, the major failure being conversations with Snapdeal.

A company that started in 2011, became a Unicorn in 2016 and would be shutting shop in 2019 – ShopClues. When GIC lead the Series E round in the company which took the valuation to $1.1 billion; did the projections, in any way figured in the possibility of the company going down under? No.

Does that not solidify the fact that the trending practice and methods of calculating these mighty valuations, and associating these tags with startups, unless financially justifiable, are actually pointless activities and toxic to the startup ecosystem?

If we take a look at the basic revenue & loss figures of ShopClues in FY18 – 50% increase in revenue from operations (RfO) and a 40% decrease in losses, looks like an improvement in the financials. But when we do an in-depth financial analysis – we find out that, albeit decreasing, these losses have been piling up year after year, where the funding rounds haven’t been able to keep up with the burn rate in the company.

Losses and expenses decreased because the company didn’t have enough money to spend on things that needed investment. Forget investment, the company did not have enough funds to pay off its vendors, or even its employees.

In FY18 – the major cash burn was to pay off outstanding trade payables which went down from Rs 127.08 crore in FY17 to Rs 104.5 crore in FY18. The outstanding employee payments had accumulated to Rs 1.7 crore in FY18 itself.

And, at the same time, this money was being invested in non-current and financial assets – money market, mutual funds etc to make up for the revenues that its core model failed to generate. This non-current investment went up from Rs 1.28 crore to Rs 8.81 crore. Where the company had brought Rs 33,639 worth financial assets in FY17, the investment had increased to Rs 9.69 crore in FY18.

On the other hand, ShopClues was writing off its fixed assets. In FY17 the company-owned Rs 4.03 crore worth of PPE, the value came down to Rs 2.11 crore in the next fiscal. FY16 saw this figure stands at Rs 6.84 crore.

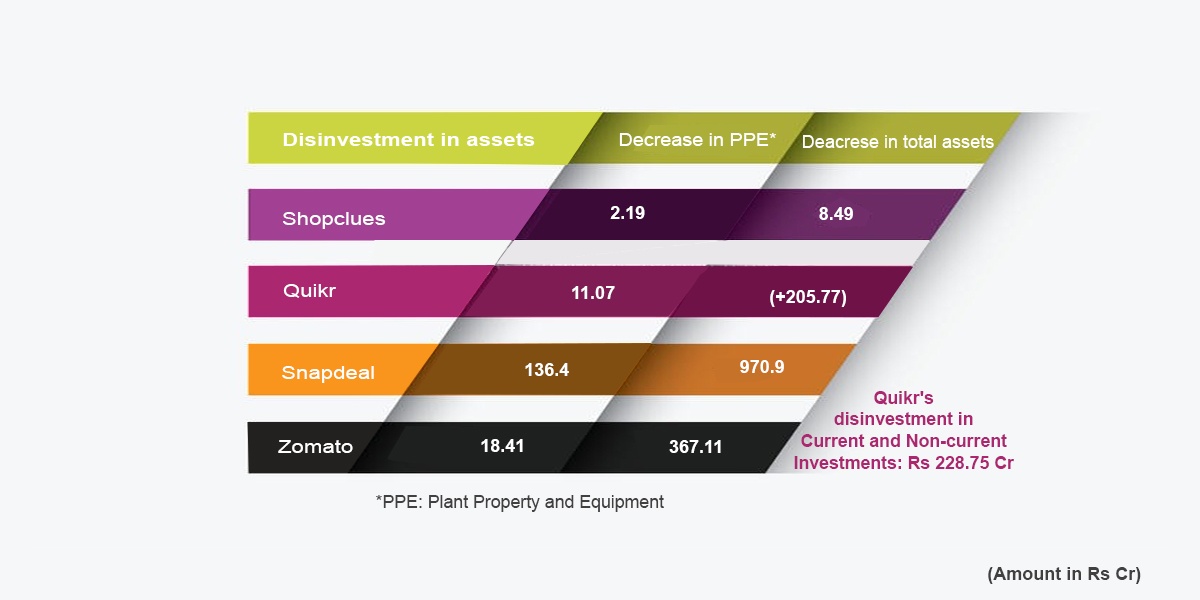

Alarmingly, disinvestment isn’t a case limited to ShopClues. Snapdeal, Zomato, and Quikr – all three have seen substantial disinvestment in FY18.

Quikr: acquisition, goodwill, and valuation

Quikr, another startup that is a testament to the saying “great cry and little wool” with 15 acquisitions, and Rs 173.49 crore worth consolidated revenue from operations after 10 years of operations, and positive cash balances only because of the sale of investment property and fixed assets. The value of PPE owned went down from Rs 33.97 crore in FY17 to Rs 22.9 crore in FY18. Non-current investments, i.e. long term investments that are not used to generate operating income, toppled down by 84.05% from Rs 31.56 crore to Rs 5.02 crore.

Even the working capital of the company took a hit as the current investments, the investments made to earn money that can be used in the working capital cycle, were slashed by Rs 202.21 crore – as they fell from Rs 361.3 crore to Rs 159.09 crore.

And this has been happening since FY17, where the company had a cash inflow of Rs 765.87 crore from sale of investment property. In FY18 the cash inflow was reduced to only Rs 248.87 crore.

The only two assets that saw an uptick were loans advanced, which went from Rs 9.34 crore to Rs 103.92 crore, and Goodwill. Goodwill – the intangible asset which takes a 13.8X jump only in rare circumstances. Like when a company goes on an acquisition spree where the amount paid for these startups is more than their Net Asset Value (NAV) or the equity invested in the firm. In FY18 itself, Quikr had acquired 4 startups – Zimmber, Babajob, HDFC Realty, HDFC Red, all being paid hefty purchase considerations much more than the NAVs they maintained. Hefty enough to take the goodwill figure from Rs 13.65 crore in FY17 to Rs 188.47 crore in FY18.

Quikr’s growth chart seems to be running on acquisitions, because the revenues of Rs 199.7 crore are definitely not even enough to cover the Rs 209.31 crore worth employee benefit expenses, forget about the overall expenses of the firm. And neither has the firm been able to secure equity funding to fund the losses.

After 2016, the firm is surviving on debt investments, leveraging the firm even further.

For some reason, since there has been no news of there being filed a legal case against Quikr, the P&L account of the firm still shows the legal and professional fee doubling to Rs 10.87 crore from Rs 5.09 crore in FY17.

Looking at all these facts it only makes sense how the valuation of the firm, calculated by Kinnevik AB – one of its investors – came down to $885 million in December 2017. However, the valuation was restored above $1 billion in the next quarterly report. Why? And how?

With this kind of financial performance in FY18, it is surprising how the investors were able to restore the valuation to over $1 billion. Projections based on such statements that add up to these mighty valuations go on to devalue the importance of financial prudentiality and somewhere raise questions around the fairness of these reports.

The online classified industry in India is in a slump, and whatever market there is, is dominated by the foreign giant OLX. Quikr, even with its dire attempts at trying to corner a significant market share for itself, and then trying to expand horizontally into home services to find a stable business model, has failed to leave a lasting mark in the market as vertical players focussing on one service have been doing better than horizontal players like Quikr.

Where OLX’s India play is limited to selling or renting appliances, houses, automobiles etc and that too only over the internet, Quikr has spread its wings in home services, jobs, classifieds, financial services, education, B2B supplier classified. The latter has even started putting up a few of its products in offline stores – QuikrBazaar – in Telangana and Karnataka for touch and feel experience prior to purchase.

The question here is not about the relevance of these forays by Quikr, but the fact that OLX India has been profitable for the past few years – Rs 15.6 crore in FY18 and Rs 8 crore in FY17, while Quikr has been piling up losses.

While India couldn’t build its Craigslist, due to the lack of both – the market potential and investor interest in the past couple years, there is one segment that has been the belle of the ball in the same duration and it boasts of not 1 but 2 unicorns – foodtech.

Foodtech unicorns

However, even with the skyrocketing market potential and the blind in-pour of funds by investors, only one of these unicorns showcases a financial report that can give credibility to its valuation. The other one, in some aspects – mostly due to miscalculated business decisions and not for the lack of a viable business model – still struggles to showcase a growth-stage business model that can be given soaring valuations.

The two names here are Swiggy and Zomato. Can you guess which is which?

Let’s look at some figures to arrive at an answer.

The reason that we see some of these figures with regards to Zomato, is that in FY18 the firm did internal financial restructuring to an asset-light model.

Unlike Swiggy, that has invested in ramping up its PPE, intangible assets, non current investments, current investments, as well as inventory to fuel expansion, and strengthen logistics; Zomato has written off more than half of its fixed assets, its goodwill slashed down from Rs 191.81 crore in FY17 to mere Rs 13.9 crore in FY 18.

The company offloaded its current borrowings entirely by paying back lenders with the fixed asset sale money and all this was done to switch to an asset-light model for greater margin on returns.

To get some perspective the value of total assets owned by Zomato went down from Rs 654.56 crore to Rs 287.45 crore – a 56.08% decrease. The firm even laid off its employees to bring efficiency in operations, as reflected by the downfall in the company’s employee benefit expenses.

In fact, the firm is still laying off employees on account of operational efficiency.

At the same time, Swiggy’s balance sheet reflected higher growth figures than Zomato. Swiggy saw its revenue from core operations take a 3.32X jump to Rs 441.99 crore, where Zomato registered an 80.6% growth in revenue from operations to Rs 332.27 crore.

Swiggy’s growth was achieved on an increase in expenses and losses, where Zomato was able to control both costs and the losses. While the former reflects the case of a company making higher investments for higher returns, Zomato’s approach shows an attempt towards making a more sustainable business, but these figures are slated to change in FY19, where the Deepinder Goyal led firm has spent drastically on discounts and cashbacks, just as Swiggy started walking away from a discount heavy business model.

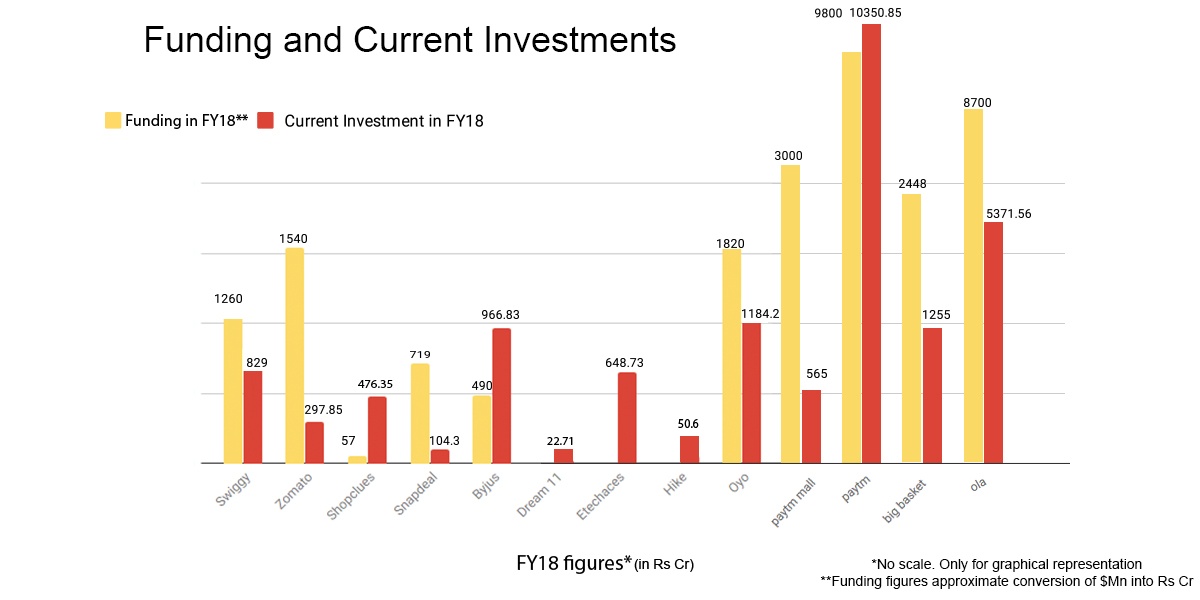

Swiggy’s FY18 financials, which must have acted as the base of the $1 billion valuation that the company achieved in June 2018, more or less justified the projections made. As far as Zomato is concerned, we wouldn’t be the first ones to question the valuation of the firm. One year after becoming a unicorn, the firm’s valuation was marked down to a half – $500 million – by HDFC Securities and Capital Markets and equity research firm Jefferies.

The reason Zomato has sustained a $1 billion valuation for the past 3 years is that the team refuses to secure funds in a down round riding on its belief in the product. Which is a great spirit, but it still doesn’t take away from the fact that valuation depends on numbers and not spirit.

Like Swiggy, several Unicorns, as they keep on receiving funding rounds, can be seen paying back long term borrowings, preferring equity financing over debt, and generally bringing a change in the leveraging of the firm. BYJU’S, OYO, BigBasket, and Snapdeal have engaged in these activities, and when we look at these companies balance sheets, the performance shows a positive flow in operations in a growing organisation, going on to explain and validate the valuations achieved.

The exceptional case of Snapdeal

Snapdeal’s case is exceptional here. After bearing drastic losses worth Rs 4,647.1 crore in FY17, the firm was at ground zero. To pick up from there and executing its turnaround story the firm took on itself the task of significantly scaling down operations and expenses to create a sustainable and economical business that focuses on a market that would lead to its growth while being able to maintain unit economics.

To execute this rise of a phoenix, the company had to write off PPE worth Rs 136.4 crore, taking the figure to Rs 71.7 crore. The goodwill was amortized to zero. Intangible assets and non current financial assets were also sold out almost completely to enable payments due to lenders and vendors, and towards increasing inventories by 39.8% to Rs 491.1 crore. Not only did the company payback 29.3% of its trade payables, it also collected 94.3 of its trade receivables and brought down the figure to Rs 4.9 crore. The transformation process did bring a dip in the company’s revenue – by 51.7% to be precise, but the 86.8% reduction in losses to Rs 613 crore was a bigger win for the company.

With all the due appreciation to the turnaround story, the company has also revealed its financial performance for FY19 and under the new regime – Snapdeal 2.0 – the company grew its revenues by 86.7% to Rs 813.8 crore and the losses further reduced by 71% to Rs 186 crore.

While the company is back on track, the fluctuations in the company’s balance sheet didn’t replicate the behaviour in the valuation of the firm. Since the recent investment in the firm by Anand Piramal was done in personal capacity the valuation of the current round is unknown yet, and is unlikely to see a change. However, given the market scenario, the magnitude of this change cannot be ascertained

Ola, Current Investment, and Paytm Family

In a financial report polar opposite of Snapdeal, Ola saw all its Balance Sheet items increase significantly. PPE increased by 72.09% to Rs 1,113.68 crore, intangible assets, trade receivables, liabilities, borrowings – each of these items saw a significant increase. One of the few items that saw a decrease was cash and cash equivalents, as the company put away money for investments and vendor payments or a plausible change in cash policy. The other items to see a decrease were the expenses and the losses of the company. Where the revenue increased by 56.87% to Rs 1,847.5 crores – majorly contributed by commission & fees, and lease rentals; the expenses saw a minor 2% decrease to Rs 5,066.58 crores, and the losses were controlled by 41.9% to Rs 2,842.26 crores.

The most interesting part of Ola’s financials is its current investments from 0 to Rs 1,445.35 crore. Current investments reflect the money allocated in mutual funds and financial securities. Investing in these instruments make way for quick and higher rewards depending on the nature and specifications of the securities or mutual funds purchased.

When the core operations aren’t sufficient for generating the target revenues and paying off vendors and other working capital requirements, current investments come in handy. But these only go on to show a trend where the large investments received from investors is being reinvested in mutual funds reducing a business to a middleman earning interests. Sometimes even the money owed to lenders and employees is being invested in these investments. The most disastrous examples of this being ShopClues. The company owes its vendors and employees, has minimal funding, but still the current investment stands mighty high.

And with growing valuations and business operations this factor doesn’t go down, the dependency on mutual funds doesn’t decrease. Case in point, Paytm – the company which is currently valued at around $18 billion, has invested the largest amount towards current investments in FY18 – Rs 10,350 crore.

Where the revenue for operations of Paytm might have taken almost a 5X jump from Rs 614.62 crore to Rs 3,058.09, this growth was riding on advertisement expenses worth Rs 2,232.79 crore and some miscellaneous expenses worth Rs 1,528.17 crore, where there is no explanation around the nature of these expenses.

Paytm’s subsidiary Unicorn – Paytm Mall, hived off in February 2017, and valued at $1 billion in April 2018, had actually disinvested in its intangible assets in FY18, and the total assets had seen a downfall of Rs 713.47 crore. The return on capital employed had gone down from -0.000816 to -4.147 as fresh capital was brought in but there wasn’t a proportionate increase in income and expenses made to drive sales were futile. Even the quick ratio, that reflects how many current assets the firm owns to pay off current liabilities in its day to day operations, went down from 2.852 to 0.955 as the company adopted a cash heavy model, purchased current investments, and trade payables rose to Rs 568.73 crore.

For a little over a year old firm, the other expenses were abnormally high at Rs 2,214.94 crore in FY18, and there were related party transactions worth Rs 757.06 crore under miscellaneous expenses. Which could imply that a significant part of the firm’s losses were due to the amount it paid to its related companies.

Looking at all this, and the fact that Paytm Mall had a negligible chance at becoming a successful B2C e-commerce marketplace, given its unsustainable cashback model and mighty competitors like Flipkart and Amazon, the restructuring going on since January this year becomes a predictable outcome. Still the company, right after the publication of this FY18 balance sheet, was given a valuation of $2 billion. Makes complete sense.

EtechAces, not PolicyBazaar

Another case that requires clarification is that, PolicyBazaar on its own is not a Unicorn. EtechAces – the parent entity that holds PolicyBazaar, PaisaBazaar, and DocPrime altogether has a valuation of over $1 billion, but not PolicyBazaar in its standalone Balance Sheet. Why are we saying so? The standalone company does not account for a single item (except the revenue that stood at Rs 159.35 crore) that was over Rs 100 crores. The independent scale of PolicyBazaar is too low for it to be a Unicorn.

EtechAces, on the other hand, by virtue of holding three companies, has achieved a scale that explains the valuation of the company. The one thing that sets its consolidated Balance Sheet apart from every other is that the company held Rs 4,099.29 crores of deferred tax assets by FY18 . The figure which represents a notional asset on the balance sheet which will be written off against taxable income in future, had taken a 3X jump from Rs 1,381.12 crore in FY17.

Dream11: customer acquisition and revenue relations

Dream11, Indian’s only gaming unicorn has a negative Net Asset Value or negative equity as it is reserving losses in its balance sheet instead of bringing in more capital to adjust these losses. But that is the case till FY18. The company has picked up $100 million from Tencent in September last year and catapulted into the Unicorn Club with a secondary investment from Steadview Capital in April this year. And by this time, the valuation of the company could have seen the difference due to these factors, along with the fact that the company had scaled up significantly in FY19.

However, a larger trend that the company’s financial statements did point out to in FY18 was that of the relation between ad, discount, and cashback expenses and the revenue that these generate for the firm. This is an important metric to look at as it reflects the viability of such revenue models used by these startups.

As we can see, for Hike, Paytm Mall, and Dream11, these promotional expenses are higher than the core revenue generated. When such is the business model, the stability of the firm’s future comes into question as to how long can a firm afford to spend in these categories, where the returns aren’t proportionate.

Zomato reflected an exceptionally sustainable customer acquisition expenses and revenue relation, however, that was the story of FY18 where the firm was going through an internal restructuring as shown by the disinvestment and profit and loss figures. In FY19, the firm has spent rivers on 50% monthly cashback schemes.

The other firm to show a proportionate growth in promotions and revenues is OYO. In fact, this firm has model financial statements that showcase a growth stage firm with positive growth in all metrics, and especially with a controlled increase in expenses. However, that was the case before the firm had spread its wings outside of India. It remains to be seen how international expansion has affected the performance of the firm. Nonetheless, based on the FY18 Balance Sheet and P&L of the firm it won’t be far fetched to say that this firm justifies its valuation.

Conclusion

Rest, as we have discussed, there are several trends in the startup ecosystem around valuations that go on to devalue the claims that these unicorns and their investors have been making for a long time. And it calls for a serious reality check.

Disinvestment by a firm to bring in money for the working capital needs is a glaring anti-growth sign that goes on to reflect prevailing financial mismanagement. Sloshing down investor money in mutual funds to again help the working capital flow only goes on to showcase a larger interest income play that accounts for a weak and unsustainable core revenue model and an opportunity cost as far as growth-oriented investment is concerned.

The advertisement and promotion expenses being greater than the revenue earned, year after year, becomes problematic as the scale that the company is looking to reach with that investment is not being delivered. From a layman’s angle, in such cases the firm is paying the customer more than the revenue this customer is generating for the firm, and when has that been optimum for any business?

The fact that these are some hard-hitting realities in not one, but many so-called unicorns, raises concerns around the valuation that firms and investors keep on boasting about and relying on for capital gains. In this long game of risk, exactly how much is worth this risk?