UPI’s popularity, adoption, and influence on digital transaction in India is the result of the government’s aggressive move to bring a unified payment railroad for mobile-based payments. Since its inception in early 2016, UPI has recorded remarkable growth, outpacing other modes of peer-to-peer-payments and engrossing a shift in peer-to-merchant payments.

Seven months before the demonetisation, NPCI conducted a pilot with 21 member banks to launch one of the most influential products in the payments industry and as a result, 142 banks have joined the UPI ecosystem since its formal launch.

The credit for initial growth in adoption by several banks already has been attributed to demonitisation. However, the next set of growth was fueled when venture capital-backed payments companies like Paytm, PhonePe and later on Google Pay joined the UPI stack.

These companies observed that UPI is the best medium to popularise digital fund transfer. They used the proven formula of cashbacks to make a shift towards using UPI over other fund transfer methods such as IMPS and NEFT.

PhonePe and BHIM were the early evangelist of UPI stack followed by Paytm, MobiKwik, Freecharge, and others. It’s worth noting that currently – Paytm, PhonePe and Google Pay collectively drive more than 90% of UPI transaction.

On the other hand, because of its sheer simplicity and easy UX for transfers, UPI faced no friction in attracting already internet-friendly users as well as new users ripe for adopting electronic fund transfer post demonitisation.

Comprehensive comparison of UPI growth since 2018

NPCI’s foolproof planning before opening up UPI to masses can be testified with the product’s quick acceptance across cities irrespective of size and economic conditions.

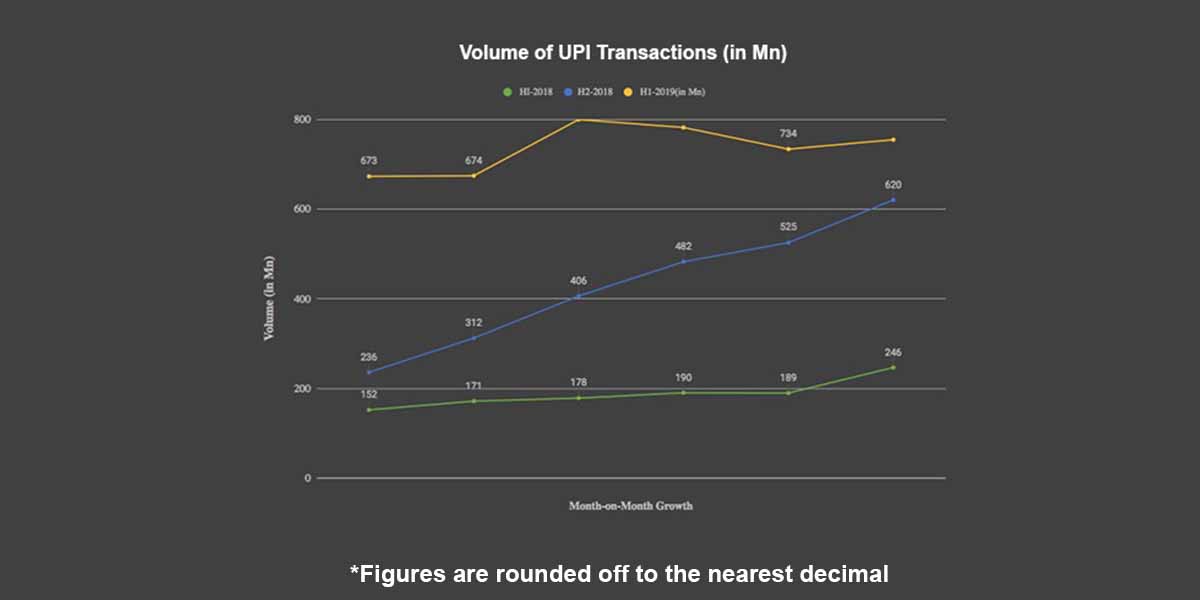

To understand the growth of UPI, let’s compare the figures for H1-2018 (Jan to June) with H2-2018 (July to Dec) and H1-2019 (Jan to June).

In January 2018, UPI transaction volume stood at 151.8 million with a total value of Rs 15,571.20 crore. It recorded a 63% spike in volume and 162% rise in the value of the transaction as of June 2018.

Similarly, we can see collective growth between July 2018 to December 2018, the increase in volume and value recorded at 163% and 123% respectively.

Further in January 2019, the volume figure was recorded at 672.75 million transactions while the value of these transactions peaked to Rs 1,09,932.43 crore. This saw a mere 12% hike in volume and 33% rise in value as June 2019 was recorded at about 754.54 million transactions worth Rs 1,46,566.35 crore.

So, H1 2018 saw 63% and 162% increase in volume and value respectively whereas H2 2018 registered 163% and 123% increase in volume and value. The figure gradually becomes stagnant in H1 2019 as UPI recorded 12% and 33% rise in volume and value respectively.

Not only UPI, other electronic payments systems such as NEFT, RTGS, IMPS also saw a spike in transaction volume. Meanwhile, UPI had achieved a milestone of executing close to 800 million transactions in March and clocked Rs 1.5 trillion worth transaction for the first time in May 2019.

After Paytm, Google Pay leads the pack in UPI ecosystem

Paytm was claiming pole position in the UPI ecosystem till February this year. However, Google Pay and Flipkart-owned PhonePe have been scoring lead over the Alibaba-backed company ever since.

In May, Google Pay had recorded 240 million transactions amounting to Rs 55,000 crore whereas PhonePe and Paytm registered 230 million and 200 million transactions worth Rs 44,000 crore and Rs 38,200 crore respectively.

The next set of plans for UPI is doubling down on merchant payments as these have continually increased in the past few months – 15% in April to 31% in June. About 240 million merchant payments were processed via UPI in June 2019. For perspective, this volume is almost equal to Google Pay’s overall UPI transactions.

Entrackr has sent queries to NPCI requesting UPI-based merchant payments data. However, we’re yet to hear from the corporation.

BHIM losing plot

While overall UPI and private players market share increased tremendously, government-regulated BHIM has been losing its luster and barely processes 2% transactions in UPI ecosystem. Below graph shows that BHIM has been hovering at 15 million transaction for the past 6 months.

Lack of focus, promotion and anti-cashback thesis seems to have choked BHIM’s growth.

Has UPI reached its saturation point?

The fate of BHIM lies in the hands of the government and a further push isn’t likely given the presence of deep-pocketed private players. Likewise, UPI has also seen ups and downs in 2019. In a nutshell, UPI’s average growth in the last six months has been flat (except March and April).

This is because these numbers are closely dependent on Paytm, Google Pay, and PhonePe. It’s anticipated that this growth will slow down even further and is even slated to take a dip as Paytm is shifting its focus on merchant-based incentives.

“We will not drive promotions on UPI payments anymore as we can see that the user base has plateaued at 50 million,” Vijay Shekhar Sharma, the Founder, and CEO of Paytm said in an interview two weeks.ago

This will trigger downfall in transaction volume as well as value from Paytm’s side.

On the other hand, it will be worthwhile to watch for how long Google Pay and PhonePe drive the growth of UPI by throwing money on cashback. It’s likely that the trend of cashback is not going to subside as Google Pay would want to maintain its momentum and PhonePe is in conversation to raise a mega-round.

If PhonePe gets the round at a valuation it wants, cashback war would even be more fierce.

Further, saturation of UPI market is more a myth than reality considering there is still a vast market potential given how a large part of the Indian population is still devoid of this facility. It might be so that most of the current urban population using these applications has been onboarded on UPI, but a large factor still remains an unpenetrated market.

It may be too early to ascertain UPI’s future trajectory but looking at the recent info on BHIM as well as UPI itself, there is a need for improvement and incoming of more private players. The debut of deep-pocketed players such as Amazon Pay, Mi Pay, and a mass rollout of WhatsApp Pay would definitely bring new momentum to the UPI ecosystem.